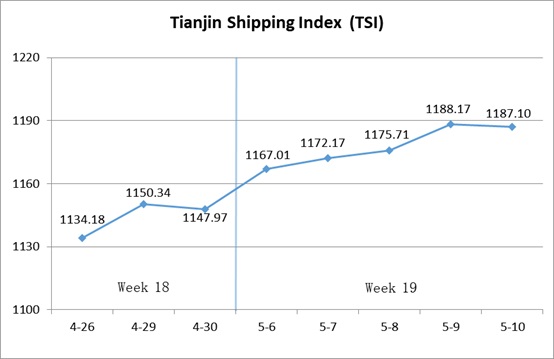

I. Tianjin Shipping Index (TSI)

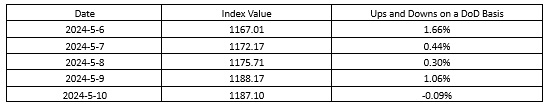

In Week 19, 2024 (May 6 to May 10), Tianjin Container Freight Index (TCI) climbed steadily. Tianjin Bulk Freight Index (TBI) continued to increase. Tianjin Domestic Container Freight Index (TDI) decreased rapidly. The TSI continued to increase, closing at 1187.10 points, with a cumulative increase of 39.13 points (3.41%) from Apr.30 (the last release day of Week 18). The trend of TSI is as follows:

The value and trend of TSI is as follows:

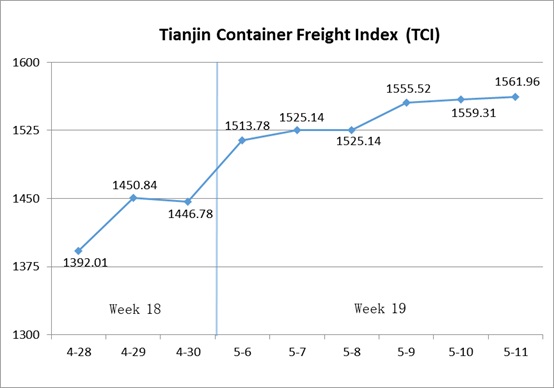

II. Tianjin Container Freight Index (TCI)

In Week 19, 2024 (May 6 to May 11), due to the five-day May Day holiday, Tianjin Container Freight Index (TCI) was released for six times, and the trend of it is as follows:

In Week 19, the TCI continued to increase.

From May 6-May 7 (Mon.-Tue.), the freight rates in European route, Mediterranean route, South American route and African route increased rapidly, and the freight rates in American route climbed slightly. After almost two years, the TCI rose to 1,500 points again, gaining nearly 80 points in two release days. Subsequently, the freight rates in European route, Mediterranean route, American route, South American route and African route increased steadily. The TCI further increased, with a cumulative increase of 2.41% from May 8-May 11 (Wed.-Sat.).

Finally, the TCI closed at 1561.96 points, with a cumulative increase of 115.18 points (7.96%) from Apr.30 (the last release day of Week 18).

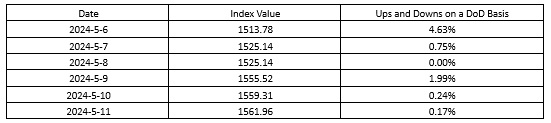

The TCI index value and several ups and downs on a day-on-day basis are as follows:

European/Mediterranean route In May, due to concerns about the delays and congestion caused by ship rerouting, importers increased their inventory replenishment efforts, and the demand for market freight rose accordingly. After the long holiday, shipping companies once again implemented a new round of freight rate increases, with freight rates continuing to remain strong. The freight indices in European route, Mediterranean East route and Mediterranean West route closed at 1246.49 points, 1579.39 points and 1931.03 points, with the increase of 12.92%, 5.92% and 8.06% this week.

American route Recently, some shipping companies reduced their schedules, coinciding with the negotiation period for long-term freight rates. Shippers demonstrated a clear willingness to maintain or raise freight rates, and freight rates continued to increase this week. The freight indices in American West Coast route and American East Coast route closed at 1419.60 points and 1371.07 points, with the increase of 3.26% and 4.07% this week.

South American route To avoid tight capacity during the peak season, local companies procured goods ahead of time, resulting in the continuous heating up of freight demand in the market. Additionally, the recent shortage of empty containers had not yet been alleviated, leading carriers to continue raising freight rates.

The freight indices in South American West route, South American East route and Central and South American route closed at 1651.82 points, 2599.79 points and 1614.89 points, with the increase of 9.44%, 15.26% and 14.63% this week.

African route As the local area entered the consumption peak season, importers increased their procurement of machinery, infrastructure, and textile and daily necessities. However, there was a shortage of available spots in the market for immediate shipping, leading shipping companies to continuously increase General Rate Increases (GRI) and Peak Season Surcharges (PSS), among others. The freight indices in South African route, East African route and West African route closed at 1941.59 points, 1735.44 points and 1880.85 points, with the increase of 22.62%, 14.39% and 31.09% this week.

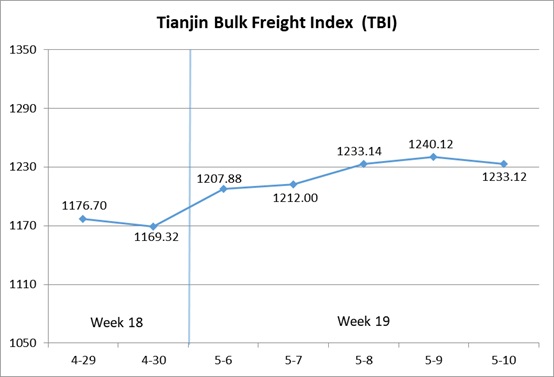

III. Tianjin Bulk Freight Index (TBI)

In Week 19, 2024 (May.6 to May.10), the trend of Tianjin Bulk Freight Index (TBI) is as follows:

In Week 19, the TBI fluctuated and decreased slightly at the latter period of the week.

On May 6 (Mon.), the freight rates of grain, coal and metal all increased compared with the day that before Labour Day, which drove the TBI to increase 3.30% on a day-on-day basis. On May 7 to May 9 (Tue. to Thur.), the freight rate of grain fluctuated and increased and the freight rates of coal and metal increased continuously, which drove the TBI to further rise with a cumulative increase of 2.67% on three consecutive releasing days.

On May 10 (Fri.), the freight rate of grain increased slightly and the freight rates of coal and metal decreased slightly, which drove the TBI to decrease 0.56% on a day-on-day basis. Compared with April 30 (the last releasing day of Week 18), The TBI finally closed at 1233.12 points with a cumulative increase of 63.80 points (5.46%).

TBI index value saw several ups and downs on a day-on-day basis, which is shown as follows:

TBCI Showed a upward trend. Compared to April 30 (the last releasing day of the Week 18), the index value finally closed at 960.88 points with a cumulative increase of 64.68 points (7.22%). For Handymax vessels, Indonesian coal pallets transactions turn positive before and after the holiday. The freight rate of Indonesia to Qingdao route continued to rise with a cumulative increase of 2.10%. For Capesize vessels, the market freight increased significantly and the freight rate of Hay Point to Qingdao route rose with a cumulative increase of 10.55% this week.

TBGI Fluctuated and increased. Compared to April 30 (the last release day of Week 18), the index value finally closed at 1050.77 points with a cumulative increase of 13.40 points (1.29%). The Panamax vessel spot capacity reduced, there was an increase in South American soybean pallets transactions and the market freight further increased. The freight rate of South America to Tianjin route cumulatively increased 2.04%, the freight rate of U.S. Gulf to Tianjin route rose with a cumulative increase of 0.53% and the freight rate of West America to Tianjin route rose with a cumulative increase of 2.00% this week.

TBMI Increased continuously at the beginning of the week and decreased slightly at the latter period of the week. Compared to April 30 (the last releasing day of Week 18), the index value finally closed at 1687.70 points with a cumulative increase of 113.32 points (7.20%). In term of the iron ore, there was an increase in iron ore pallets transaction. Coupled with increase of FFA freight, shipowners were strongly willing to support the market freight. The freight rate on route from West Australia to northern China rose with a cumulative increase of 8.97%. Pallets trading in Brazil were weak. The freight rate of Brazil to Tianjin route rose with a cumulative increase of 3.57%. In Nickel mining market, there was an increase in nickel mining pallets transactions. The freight rate on route from Surigao to Tianjin further rose with a cumulative increase of 3.37%.

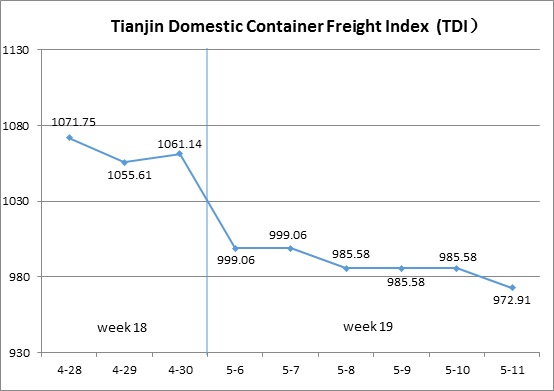

IV. Tianjin Domestic Container Freight Index (TDI)

In Week 19 (May.6 to May.11), due to the May Day holiday arrangement, Tianjin Domestic Container Freight Index (TDI) was released 6 times, the trend is shown in the chart below:

In the 19th week, Tianjin Domestic Container Freight Index (TDI) showed a sharp decline.

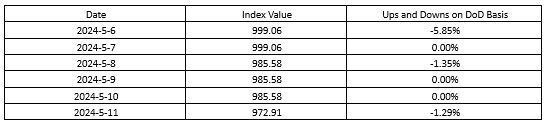

On May 6th (Monday), the inbound index slightly increased, while the outbound index significantly decreased, dragging down the TDI significantly, with a day-on-day decrease of 5.85%. Subsequently, the inbound and outbound indices stabilized. From the 8th to the 11th (Wednesday to Saturday), the inbound index continued to remain stable, while the outbound index fell twice. The TDI continued its downward trend, ultimately falling below 1000 points and closing at 972.91 points. Compared to April 30th (the last release day of the 18th week), it has fallen 88.23 points, with a cumulative decrease of 8.31%.

The TDI index value and several ups and downs on a day-on-day basis are as follows:

The Tianjin Domestic Container Outward Freight Index (TDOI) Continued to decline significantly, closing at 787.62 points on May 11th, a cumulative decrease of 205.10 points or 20.66% compared to April 30th (the last release day of the 18th week). Affected by heavy rainfall, it was difficult to clear inland ports in Guangdong, and market shipments were temporarily suspended. South China freight rates have dropped significantly, and the Tianjin to Guangzhou route freight index closed at 688.48 points, with a cumulative decline of 27.61% this week. Fujian freight rates have slightly declined, with the Quanzhou/Xiamen route freight index closing at 1132.20 points, a cumulative decrease of 4.82% this week. The freight rates in East China increased significantly at the beginning of the week and then remained stable. The Tianjin to Shanghai route freight index closed at 1095.76 points, with a cumulative increase of 6.96% this week.

The Tianjin Domestic Container Inward Freight Index (TDII) Continued its upward trend, closing at 1158.19 points on May 11th, a cumulative increase of 28.63 points or 2.53% compared to April 30th (the last release day of the 18th week). After the Labor Day holiday, the market freight rates from South China, Fujian, and East China to North China continued to rise. The freight index for the Guangzhou to Tianjin route closed at 1140.11 points, with a cumulative increase of 1.37% this week; The freight index for the Quanzhou/Xiamen to Tianjin route closed at 1204.10 points, with a cumulative increase of 2.09% this week; The freight index for the Shanghai to Tianjin route closed at 1205.72 points, with a cumulative increase of 12.23% this week.

(The analysis report is for reference only and at your own risk)