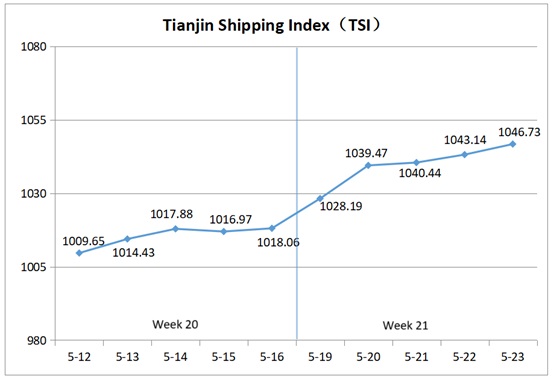

I. Tianjin Shipping Index (TSI)

In Week 21, 2025 (May 19 to May 23), Tianjin Container Freight Index (TCI) rose rapidly, Tianjin Bulk Freight Index (TBI) experienced minor fluctuations but generally increased. Meanwhile, Tianjin Domestic Container Freight Index (TDI) remained stable with a slight decline. The The Tianjin Shipping Index (TSI) continued to rise and ultimately closed at 1,046.73 points, with a cumulative increase of 28.67 points (2.82%) compared to May 16(the last release day of Week 20). The trend of TSI is as follows:

The value and trend of TSI is as follows:

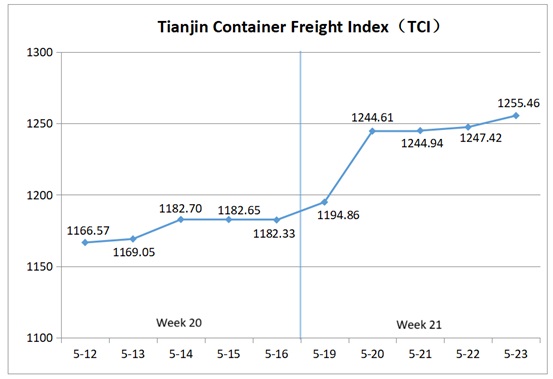

II. Tianjin Container Freight Index (TCI)

In Week 21, 2025 (May 19 to May 23), the trend of Tianjin Container Freight Index (TCI) is as follows:

In Week 21, the TCI continued to rise.

From May 19 to May 20 (Mon. to Tue.), the freight rates in European, Mediterranean, American, South American, and Persian Gulf routes all increased significantly, causing the TCI to soar and rise by a cumulative 5.27% over two consecutive release days. Subsequently, the freight rates in European, American, South American and Persian Gulf routes saw a narrowing of their increases, while the Mediterranean route's freight rates stabilized. The growth of TCI slowed, with a cumulative increase of 0.87% from May 21 to 23 (Wed. to Fri.).

Finally, the TCI closed at 1,255.46 points, with a cumulative increase of 73.13 points or 6.19% compared with May 16 (the last release day of Week 20).

The TCI index value and several ups and downs on a day-on-day basis are as follows:

The TCI includes 19 sample routes. The main route analysis of this week is as follows:

European/Mediterranean route Cargo volume was basically stable, and part of the market capacity was deployed to the American route, resulting in tight spot space on this route. Shipping companies continued to generally raise freight rates. The freight indices in the Tianjin to Europe, the East Mediterranean, and the West Mediterranean routes closed at 681.01 points, 998.79 points, and 1,306.47 points respectively, up 15.27%, 6.87%, and 6.16% week-on-week.

American route Following the ratification of the Geneva Tariff Agreement, factories and traders accelerated shipments, boosting demand. Tight vessel capacity drove rates sharply upward. The freight indices for Tianjin to American West Coast and Tianjin to American East Coast routes ended at 1,169.69 points and 1,074.06 points, with week-on-week increases of 14.32% and 11.93%, respectively.

South American route With reduced market capacity and some shipping companies imposing weight limits on small containers, shipping companies generally increased various surcharges, including the General Rate Increase (GRI), Peak Season Surcharge (PSS), and Overweight Surcharge (OWS). Freight rates rose strongly. The freight index for the Tianjin to West South America, East South America, and Central South America routes closed at 871.07 points, 996.74 points, and 1,270.42 points, respectively, with weekly increases of 18.84%, 14.14%, and 44.58%

Persian Gulf route Steady demand growth and limited spot space propelled rates upward. The freight index of this route closed at 830.80 points, with a week-on-week increase of 11.39%.

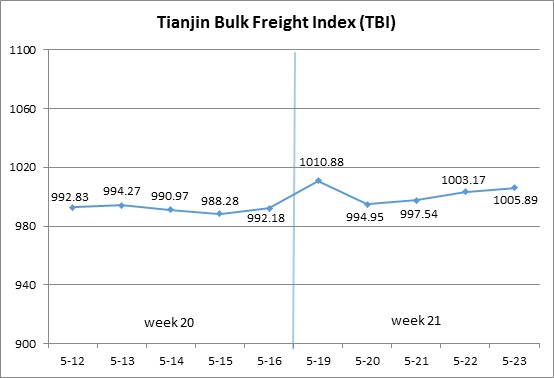

III. Tianjin Bulk Freight Index (TBI)

In Week 21, 2025 (May 19 to May 23), the trend of Tianjin Bulk Freight Index (TBI) was released as shown as follows:

In Week 21, the TBI fluctuated and decreased.

From May 19 to 20 (Mon. to Tue.), grain market freight rates continued to decline, while coal and metal ore market freight rates first rose and then fell. TBI showed a fluctuating trend, with a cumulative increase of 0.28% over the two release days. Subsequently, grain market freight rates further declined, while coal and metal ore market freight rates continued to rise slightly. TBI rose slightly from May 21 to 23 (Wed. to Fri.) and finally closed at 1005.89 points, a cumulative increase of 13.71 points or 1.38% compared to May 16 (the last release day of Week 20).

The TBI index value and several ups and downs on a day-on-day basis are as follows:

TBCI Closed at 754.07 points, a cumulative increase of 6.80 points or 0.91% compared to May 16 (the last release day of Week 20). Coal import pallets are limited, and there is a differentiation in freight rates among different ship types. In terms of the Supramax market, the available capacity has increased, and the freight index for the Indonesia to Qingdao route has slightly decreased by 0.04% on a weekly basis. In terms of the Capsize market, freight rates in the Pacific region fluctuated and rose, with the freight index of the Hay Point to Qingdao route rising 1.53% week on week.

TBGI Closed at 877.89 points, a cumulative decrease of 0.67 points or 0.08% compared to May 16 (the last release day of Week 20). The overall capacity of Panamax ships is abundant, and some of the capacity is empty for cargo collection in South America. The demand for grain transportation in South America is basically stable, and market freight rates have continued to decline slightly. The freight index for the South American to Tianjin route decreased by 0.04% on a weekly basis, the freight index for the US Gulf to Tianjin route decreased by 0.09% on a weekly basis, and the freight index for the US West to Tianjin route decreased by 0.12% on a weekly basis.

TBMI Closed at 1385.72 points, a cumulative increase of 35.02 points or 2.59% compared to May 16 (the last release day of Week 20). In terms of iron ore, the increase in transactions of Australian and Brazilian miners last weekend pushed up freight rates. However, due to the increase in transportation capacity and the cancellation of mining rights in West Africa, freight rates significantly declined. In the second half of the week, the market's cargo trade continued, consuming available transportation capacity, and freight rates rebounded again. The freight index for the route from Western Australia to Northern China increased by 3.94% on a weekly basis, while the freight index for the route from Brazil to Tianjin slightly decreased by 0.30% on a weekly basis. In terms of nickel ore, there are few transactions of nickel ore in the Philippines, and the market capacity supply exceeds demand. The freight index of the Surigao to Tianjin route fell by 0.10% on a weekly basis.

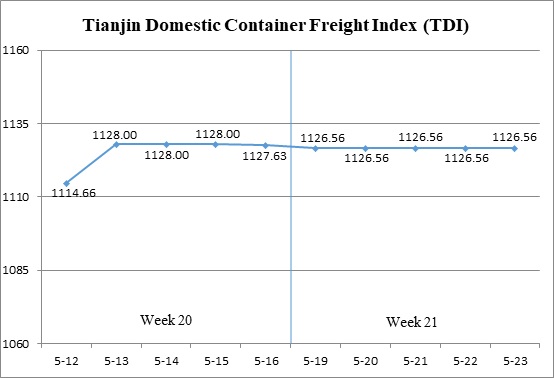

IV. Tianjin Domestic Container Freight Index (TDI)

In Week 21 (May 19 to May 23), the trend of the Tianjin Domestic Container Freight Index (TDI) is shown in the chart below:

During Week 21, the Tianjin Domestic Container Freight Index experienced a slight pullback.

On May 19 (Mon.), the inbound index saw a small decline, while the TDI dropped slightly. From May 20 to 23 (Tue. to Fri.), the inbound index stabilized, and the outbound index remained steady throughout the week. As a result, the TDI ended the week at 1126.56 points, marking a cumulative drop of 1.07 points (or 0.09% ) compared to May 16 (the last release day of Week 20).

The TDI index value and several ups and downs on a day-on-day basis are as follows:

The Tianjin Domestic Container Outward Freight Index (TDOI) Remained stable, closing at 1126.56 points on May 23, unchanged compared to May 16 (the last release day of Week 20). The coal transport market entered the off-season, while steel orders shifted towards foreign trade. This resulted in insufficient volume in the domestic market. As a result, outbound freight rates from Tianjin remained stable. The freight index for the Tianjin to Guangzhou route, Tianjin to Quanzhou/Xiamen route, and Tianjin to Shanghai route closed at 1053.44 points, 1162.66 points, and 1135.83 points, respectively, with no weekly change.

The Tianjin Domestic Container Inward Freight Index (TDII) Experienced a slight decline, closing at 1176.69 points on May 23, down by 2.14 points (a 0.18% decrease) compared to May 16 (the last release day of Week 20). Widespread rainfall in southern regions affected the shipment of building materials, while fertilizer transport entered the off-season. The volume of household appliances and ceramics remained stable. Freight rates in the East and South China markets remained steady. The Shanghai to Tianjin route and Guangzhou to Tianjin route closed at 1061.42 points and 1250.66 points, respectively. In the Fujian market, freight rates slightly decreased, with the Quanzhou/Xiamen to Tianjin route closing at 944.85 points, marking a 1.24% decrease from the previous week.

(The analysis report is for reference only and at your own risk)