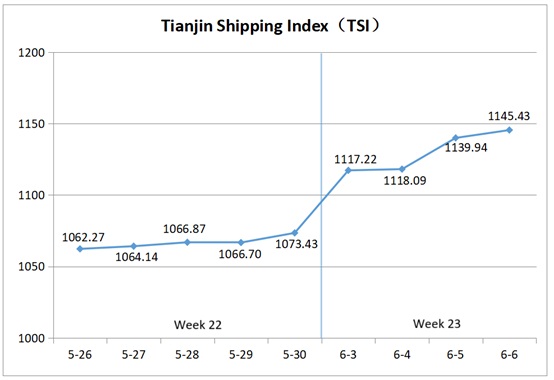

I. Tianjin Shipping Index (TSI)

In Week 23, 2025 (June 3 to June 6), the Tianjin Shipping Index (TSI) was released four times due to the Dragon Boat Festival holiday schedule. Tianjin Container Freight Index (TCI) rose sharply, Tianjin Bulk Freight Index (TBI) continued to climb, Tianjin Domestic Container Freight Index (TDI) remained stable. The TSI rose consecutively and finally closed at 1145.43 points, with a cumulative increase of 72.00 points (6.71%) compared to May 30 (the last release day of Week 22). The trend of TSI is as follows:

The value and trend of TSI is as follows:

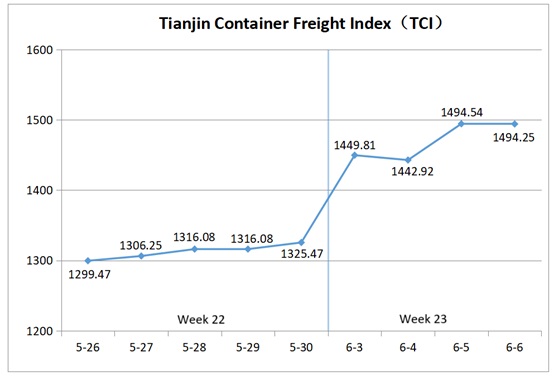

II. Tianjin Container Freight Index (TCI)

In Week 23, 2025 (June 3 to June 6), the trend of Tianjin Container Freight Index (TCI) is as follows:

In Week 23, the TCI saw a significant increase.

From June 3 to June 5 (Tue. to Thur.), the freight rates of the Europe, Mediterranean, American, South America, and India routes surged strongly, causing the TCI to climb significantly, with the index value increasing by nearly 170 points over the three release days. On June 6 (Fri.), the freight rate of the South America West route fell slightly, while the freight rates of the other routes remained stable, resulting in a slight decrease in the TCI, with a week-on-week decrease of 0.02% on that day.

Finally, the TCI closed at 1494.25 points, with a cumulative increase of 168.78 points compared to May 30 (the last release day of Week 22), a cumulative increase of 12.73%.

The TCI index value and several ups and downs on a day-on-day basis are as follows:

The TCI includes 19 sample routes. The main route analysis of this week is as follows:

European/Mediterranean route Strikes and weather factors caused continuous congestion at major local ports such as Rotterdam, Antwerp, and Bremerhaven. In addition, some direct shipping capacity was adjusted to other routes, and the Mediterranean route restricted the loading of high-box goods. As a result, the market freight rate surged this week. The freight indices for Tianjin to Europe, Tianjin to Mediterranean East, and Tianjin to Mediterranean West routes closed at 839.40 points, 1350.05 points, and 1730.42 points respectively, up 24.47%, 17.02%, and 15.28% week-on-week.

American route Shippers’ shipment volume remained high, and the freight rate increased more sharply this week. The freight indices for Tianjin to West America and Tianjin to East America routes closed at 1835.50 points and 1504.78 points respectively, up 30.77% and 20.56% week-on-week.

South American route Tight vessel space and advance bookings by some traders due to export front-loading, coupled with congestion at transshipment ports caused by a sudden surge in cargo volumes, led shipping companies to broadly increase General Rate Increases (GRI), Peak Season Surcharges (PSS), and FAK rates. As a result, the freight rates soared dramatically. The freight indices for Tianjin to West South America, East South America, and Central/South America routes closed at 1901.80 points, 1632.59 points, and 2087.97 points, respectively, with week-on-week increases of 83.13%, 46.23%, and 36.67%.

Persian Gulf route Shipping capacity remained tight, and carriers strictly enforced cargo weight restrictions. The route’s freight index closed at 963.34 points, a week-on-week increase of 6.62%.

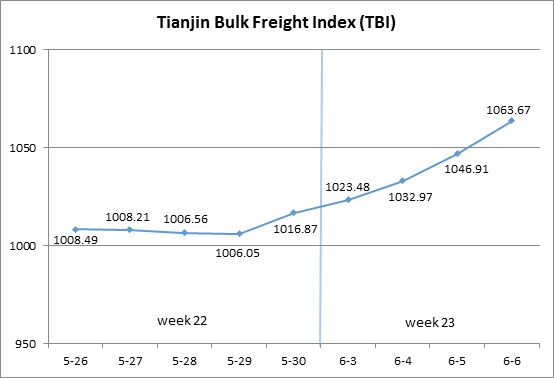

III. Tianjin Bulk Freight Index (TBI)

In Week 23, 2025 (June 3 to June 6), the trend of Tianjin Bulk Freight Index (TBI) was released as shown as follows:

In Week 23, the TBI increased continuously.

From June 3 to June 5 (Tue. to Thur.), the coal market freight rates slightly increased, the grain market freight rates continued to decline, and the metal ore market freight rates rose sharply. The total increase in TBI over the three release days was 2.95%. Subsequently, the grain market freight rates stopped falling and rebounded, while the coal and metal ore market freight rates further rose, driving TBI to climb again on June 6 (Fri.) and eventually close at 1063.67 points, with a cumulative increase of 46.80 points or 4.60% compared to May 30 (the last release day of Week 22).

The TBI index value and several ups and downs on a day-on-day basis are as follows:

TBCI Closed at 781.85 points, a cumulative increase of 22.29 points or 2.93% compared to May 30 (the last release day of Week 22). In terms of the Supramax market, the demand for coal transportation in Indonesia remained weak. This week, the freight index for the Indonesia to Qingdao route fluctuated narrowly, with a week on week decline of 0.11%. In terms of the Capsize market, the overall rate has risen, driving a significant increase in the freight index of the Hay Point to Qingdao route, with a week on week increase of 4.81%.

TBGI Closed at 870.41 points, a cumulative decrease of 2.57 points or 0.29% compared to May 30 (the last release day of Week 22). South American soybean pallets continued to be released, but there was still an excess of Panamax shipping capacity, and overall market freight rates remained weak, stabilizing slightly in the later part of the week. The freight index for the South American to Tianjin route decreased by 0.84% on a weekly basis, while the freight index for the West American to Tianjin route decreased by 0.58% on a weekly basis. In contrast, the freight index for the route from US Gulf to Tianjin increased by 0.15% on a weekly basis.

TBMI Closed at 1538.74 points, a cumulative increase of 120.67 points or 8.51% compared to May 30 (the last release day of Week 22). In terms of iron ore, Australian miners accelerated their shipment pace and rented a large amount of market capacity. The transportation demand in Brazil also increased, supporting a significant rise in market freight rates. The freight index for the Western Australian to Northern China route increased by 9.42% week on week, and the freight index for the Brazil to Tianjin route increased by 10.28% week on week. In terms of nickel mines, the weather in the Philippines improved, and there was an increase in nickel ore pallet transactions. However, there was a clear surplus of market capacity, and the freight index for the Surigao to Tianjin route declined by 0.77% week on week.

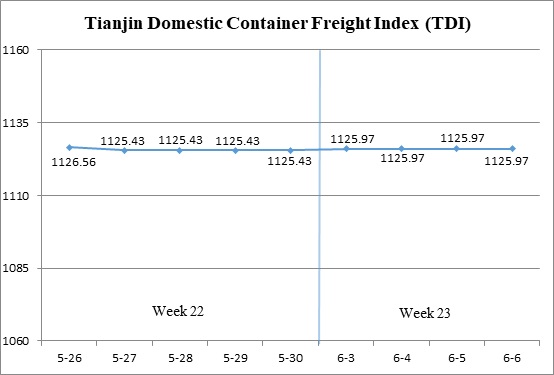

IV. Tianjin Domestic Container Freight Index (TDI)

In Week 23 (June 3 to June 6), the trend of the Tianjin Domestic Container Freight Index (TDI) is shown in the chart below:

During Week 23, the Tianjin Domestic Container Freight Index remained stable.

The outbound index held steady throughout the week, while the inbound index saw a slight uptick on June 3 (Tue.), before returning to a stable level. As a result, the TDI closed at 1125.97 points, reflecting a marginal increase of 0.54 points, or 0.05%, compared to May 30 (the last release day of Week 22).

The TDI index value and several ups and downs on a day-on-day basis are as follows:

The Tianjin Domestic Container Outward Freight Index (TDOI) Remained stable, closing at 1076.42 points on June 6, unchanged from May 30 (the last release day of Week 22). As the shipping market entered the off-season, domestic container freight rates for outbound shipments from Tianjin held steady. The freight indices for the Tianjin to Guangzhou, Tianjin to Quanzhou/Xiamen, and Tianjin to Shanghai routes closed at 1053.44 points , 1162.66 points and 1135.83 respectively, with no change on a week-over-week basis.

The Tianjin Domestic Container Inward Freight Index (TDII) Posted a slight increase, closing at 1175.51 points on June 6, up 1.07 points or 0.09% compared to May 30 (the last release day of Week 22). Freight rates in the Fujian market showed signs of recovery, with the freight index in Quanzhou/Xiamen to Tianjin route rising to 938.30 points, a week-on-week increase of 0.64%. Meanwhile, rates in the East and South China markets remained steady. The freight indices in Shanghai to Tianjin and Guangzhou to Tianjin routes closed at 1061.42 points and 1250.66 points respectively, both unchanged from the previous week. (The analysis report is for reference only and at your own risk)

(The analysis report is for reference only and at your own risk)