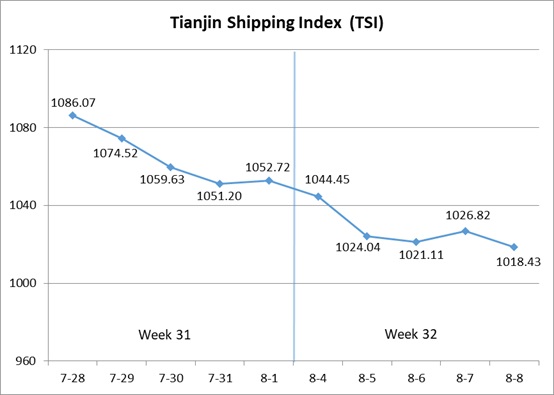

I. Tianjin Shipping Index (TSI)

In Week 32, 2025 (Aug.4 to Aug.8), Tianjin Container Freight Index (TCI) continued to decrease. Tianjin Bulk Freight Index (TBI) fluctuated downwards. Tianjin Domestic Container Freight Index (TDI) decreased significantly. The TSI continued to decrease, eventually closing at 1018.43 points, with a cumulative decrease of 34.29 points or 3.26% from Aug.1 (the last release day of Week 31). The trend of TSI is as follows:

The value and trend of TSI is as follows:

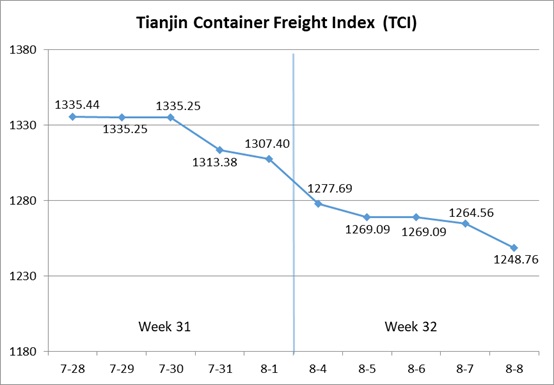

II. Tianjin Container Freight Index (TCI)

In Week 32, 2025 (Aug.4 to Aug.8), the trend of Tianjin Container Freight Index (TCI) is as follows:

In Week 32, the TCI continued to decrease.

From Aug.4-Aug.6 (Mon.-Wed.), the freight rates in European route, Mediterranean route, American route, South American East route, Central and South American route and Indian route decreased, and the freight rate in South American West route continued to increase. The TCI continued to decrease, with a cumulative decrease of 2.93% on three releasing days. From Aug.7-Aug.8 (Thur.-Fri.), the freight rates in European route, Mediterranean route, American route, South American route and Indian route continued to decrease. The TCI continued to decrease, with a cumulative decrease of 1.60% on two releasing days.

Finally, the TCI closed at 1248.76 points, with a cumulative decrease of 58.64 points (4.49%) from Aug.1 (the last release day of Week 31).

The TCI index value and several ups and downs on a day-on-day basis are as follows:

The TCI includes 19 sample routes. The main route analysis of this week is as follows:

European/Mediterranean route Due to insufficient market shipments, shipping companies increased the loading weight limit for small containers, offered discounted shipping spaces, intensified efforts to attract cargo, and freight rates showed a downward trend. The freight indices in European route, Mediterranean East route and Mediterranean West route closed at 991.74 points, 980.95 points and 1300.58 points, with the decrease of 5.87%, 7.95% and 1.06% on a week-on-week basis.

American route Due to sluggish demand for booking space in the market, shipping companies reduced the number of voyages and adjusted their capacity, resulting in a further decline in freight rates this week. The freight indices in American West Coast route and American East Coast route closed at 775.01 points and 822.36 points, with the decrease of 4.28% and 6.05% on a week-on-week basis.

South American route On the South American West route, the adjustment of capacity to meet booking demand showed results, with the freight rate slightly increasing this week. The freight index closed at 1070.64 points, with the increase of 1.85% on a week-on-week basis. On the South American East route, affected by the continuous rise in the freight rate, market capacity supply increased, and cargo owners had a strong wait-and-see sentiment. This week shipping companies lowered freight rates to attract cargo sources, and the freight index closed at 2203.86 points, with the decrease of 13.93% on a week-on-week basis. On the Central and South American route, the freight rate continued to decrease this week, with some shipping companies increasing heavy cargo rates. The freight index closed at 1384.41 points, with the decrease of 2.77% on a week-on-week basis.

Indian route The market cargo volume was weak, especially the shortage of light cargo, and the freight rate was under pressure and declining. The freight index closed at 865.82 points, with a cumulative decline of 4.23% during the week. As the local festival consumption season in India approached, the market expected a recovery, and shipping companies might push up the freight rate.

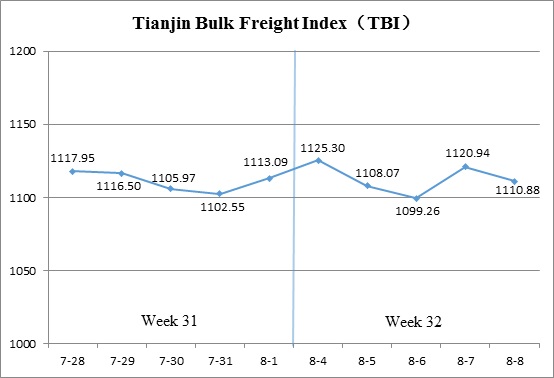

III. Tianjin Bulk Freight Index (TBI)

In Week 32, 2025 (August 4 to August 8), the trend of Tianjin Bulk Freight Index (TBI) was released as shown as follows:

In Week 32, the TBI fluctuated within a narrow range.

On August 4 (Mon.), freight rates in the grain market recorded a slight decline, while freight rates in the coal and metal ore market rates continued their rebound, pushing the TBI up by 1.10% day on day. Thereafter, freight rates in the grain market remained weak, and freight rates in the coal and metal ore market shifted from gains to losses, leading the TBI to post two consecutive days of modest declines on August 5 and 6 (Tue. to Wed.), with a cumulative drop of 2.31%. From August 7 to 8 (Thur. to Fri.), freight rates in the coal and metal ore market moved within a narrow range, while metal ore market rates experienced wider fluctuations. The TBI rose initially before retreating, ultimately closing at 1,110.88 points, down 2.21 points (0.20%) compared to August 1 (the last release day of Week 31).

The TBI index value and several ups and downs on a day-on-day basis are as follows:

Tianjin Bulk Coal Freight Index (TBCI) Closed at 836.78 points, up 3.65 points (0.44%) compared to August 1 (the last release day of Week 31). In the Supramax segment, coal cargo transactions in Southeast Asia remained steady, while typhoon-related disruptions constrained vessel availability, driving the Indonesia-Qingdao route freight index up 0.74% week on week. In the Capesize segment, the Hay Point-Qingdao route freight index fluctuated within a narrow range, posting a weekly gain of 0.26%.

Tianjin Bulk Grain Freight Index (TBGI) Closed at 928.06 points, down 2.37 points (0.25%) compared to August 1 (the last release day of Week 31). At the start of the week, freight rates in the grain market remained under pressure. In the latter half, a slight increase in Pacific coal cargoes and South American grain shipments supported a stabilization and rebound in market rates. The South America-Tianjin route freight index rose 0.13% week on week, while the U.S. Gulf–Tianjin and U.S. West Coast–Tianjin routes recorded weekly declines of 0.56% and 0.09%, respectively.

Tianjin Bulk Mineral Freight Index (TBMI) Closed at 1,567.80 points, down 7.91 points (0.50%) compared to August 1 (the last release day of Week 31). In the iron ore market, trading activity was relatively healthy early in the week, and tight spot vessel availability helped extend the rebound seen at the end of the previous week. However, a decline in FFA forward contract prices subsequently weighed on sentiment, prompting a slight pullback in freight rates. Later in the week, increased activity from both Australian and Brazilian miners supported a recovery in rates. The Australia-Western China route freight index fell 0.98% week on week, while the Brazil-Tianjin route rose 0.84%. Nickel ore shipments remained steady overall, with the Surigao-Tianjin route freight index inching up 0.07% week on week.

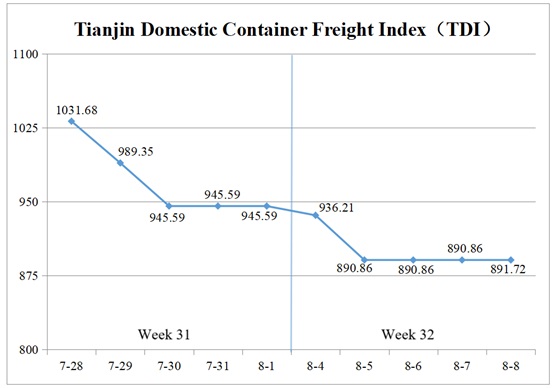

IV. Tianjin Domestic Container Freight Index (TDI)

In Week 32, 2025 (August 4 to 8), the trend of the Tianjin Domestic Container Freight Index (TDI) is shown in the chart below:

During Week 32, the decline in the TDI narrowed slightly.

From August 4 to 5 (Mon. to Tue.), the outbound index showed a slight increase, while the inbound index continued to decline, leading to a significant drop in the TDI. From August 6 to 7 (Wed. to Thur.), both the outbound and inbound indices stabilized. On August 8 (Fri.), the outbound index saw a modest rise, while the inbound index remained steady. The TDI finally closed at 891.72 points, down 53.87 points, or 5.70%, compared to August 1 (the last release day of Week 31).

The TDI index value and several ups and downs on a day-on-day basis are as follows:

The Tianjin Domestic Container Outward Freight Index (TDOI) Saw a slight increase, closing at 962.05 points on August 8, up 3.77 points, or 0.39%, compared to August 1 (the last release day of Week 31). Space remained tight for shipments from Tianjin to Fujian, driving continued freight increases. The freight index for the Tianjin to Quanzhou/Xiamen route closed at 1104.99 points, up 2.33% week-on-week. Meanwhile, freight rates for the Tianjin to Guangzhou and Tianjin to Shanghai routes remained stable, closing at 918.81 points and 1110.30 points, respectively, both unchanged from the previous week.

The Tianjin Domestic Container Inward Freight Index (TDII) Saw a narrowing decline, closing at 821.38 points on August 8, down 111.51 points or 11.95%, compared to August 1 (the last release day of Week 31). Typhoons and rainfall impacted booking demand, leading to a significant drop in freight rates. Freight rates from South China showed a smaller decline compared with the previous week, with the Guangzhou to Tianjin route index closing at 862.47 points, down 11.33% week-on-week Freight rates from Fujian continued to drop sharply, reaching a historical low, with the Quanzhou/Xiamen to Tianjin route index closing at 523.66 points, down 25.43% week-on-week. The East China market remained stable, with the Shanghai to Tianjin route index closing at 1061.42 points, unchanged from the previous week.

(The analysis report is for reference only and at your own risk)