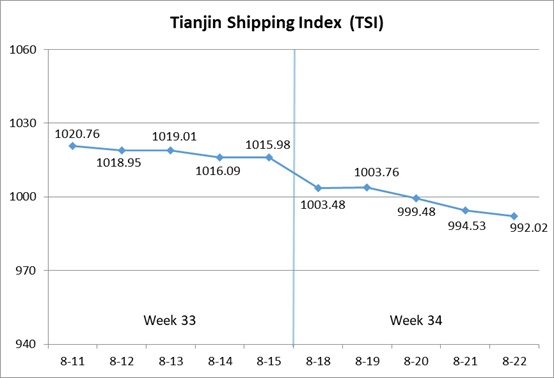

I. Tianjin Shipping Index (TSI)

In Week 34, 2025 (Aug.18 to Aug.22), Tianjin Container Freight Index (TCI) continued to decrease. Tianjin Bulk Freight Index (TBI) continued to decrease. Tianjin Domestic Container Freight Index (TDI) decreased slightly. The TSI continued to decrease, eventually closing at 992.02 points, with a cumulative decrease of 23.96 points or 2.36% from Aug.15 (the last release day of Week 33). The trend of TSI is as follows:

The value and trend of TSI is as follows:

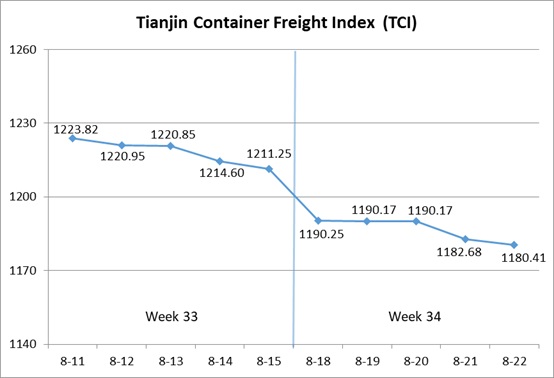

II. Tianjin Container Freight Index (TCI)

In Week 34, 2025 (Aug.18 to Aug.22), the trend of Tianjin Container Freight Index (TCI) is as follows:

In Week 34, the TCI continued to decrease.

From Aug.18-Aug.20 (Mon.-Wed.), the freight rates in European route, Mediterranean route, American West Coast route, South American East route and Central and South American route decreased, and the freight rates in American East Coast route, South American West route and Persian Gulf route stopped falling and rebounded. The performance of TCI was weak, with a cumulative decrease of 1.74% on three releasing days. From Aug.21-Aug.22 (Thur.-Fri.), the freight rates in European route, Mediterranean route, American route and Central and South American route decreased slightly. The freight rates in South American West route and Persian Gulf route continued to increase, and the freight rate in South American East route decreased at first and then increased. The TCI continued to decrease, with a cumulative decrease of 0.82% on two releasing days.

Finally, the TCI closed at 1180.41 points, with a cumulative decrease of 30.84 points (2.55%) from Aug.15 (the last release day of Week 33).

The TCI index value and several ups and downs on a day-on-day basis are as follows:

The TCI includes 19 sample routes. The main route analysis of this week is as follows:

European/Mediterranean route Congestion in major European ports had eased, while shipping demand remained weak, leading to a continued decline in market freight rates. The freight indices in European route, Mediterranean East route and Mediterranean West route closed at 906.08 points, 912.61 points and 1237.63 points, with the decrease of 2.73%, 3.36% and 2.23% on a week-on-week basis.

American route Freight rate trends were diverging. On the American West Coast route, overall supply exceeded demand, and the market freight rate continued to decline. The freight index closed at 711.35 points, with the decrease of 3.87% on a week-on-week basis. On the American East Coast route, shipping companies reduced the number of voyage, leading to a decrease in space supply. The market freight rate rebounded with fluctuations, and the freight rate index closed at 797.98 points, with the increase of 0.82% on a week-on-week basis.

South American route Freight rates saw mixed performance. On the South American West route, due to rainfall at the transshipment ports, space for feeder vessels was tight, and demand for booking increased. Shipping companies imposed surcharges such as the General Rate Increase (GRI), leading to a strong rise in freight rates this week. The freight rate index closed at 1060.48 points, with the increase of 11.02% on a week-on-week basis. In contrast, on the South American East route and the Central and South American route, the tight space for heavy cargo had eased, and freight rates subsequently declined. The freight rate indices for these two routes closed at 1736.88 points and 1303.12 points, with the decrease of 10.28% and 3.79% on a week-on-week basis.

Persian Gulf route Due to the reduction in market capacity supply, some shipping companies implemented freight rate increase plans. This week the freight rate saw a steady increase, with the freight rate index closing at 821.03 points, marking the increase of 2.21% on a week-on-week basis.

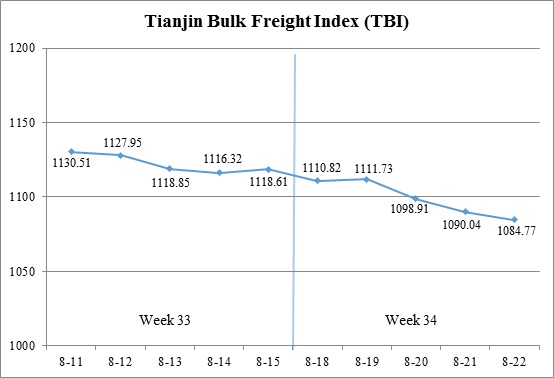

III. Tianjin Bulk Freight Index (TBI)

In Week 34, 2025 (Aug.18-Aug.22), the trend of Tianjin Bulk Freight Index (TBI) was released as follows:

In Week 34, the TBI trended downward overall.

From Aug.18-Aug.19 (Mon.-Tue.), freight rates in the grain market recorded slight gains, while freight rates in the coal and metal ore market first declined and then rebounded, leaving the TBI fluctuating lower with a cumulative drop of 0.62%. Thereafter, freight rates in the grain market continued their mild upward momentum, but sharp declines in freight rates in the coal and metal ore market weighed heavily on the market, driving the TBI to fall for three consecutive days from Aug.20-Aug. 22 (Wed.-Fri.) with a cumulative drop of 2.42%. By the end of the week, the TBI closed at 1,084.77 points, down 33.84 points (3.03%) compared to Aug.15 (the last release day of Week 33).

The TBI index value and several ups and downs on a day-on-day basis are as follows:

Tianjin Bulk Coal Freight Index (TBCI) Closed at 821.66 points, down 19.52 points (2.32%) compared to Aug.15 (the last release day of Week 33). In the Supramax segment, increased Indonesian coal shipments supported freight rates, with the Indonesia-Qingdao route index rising 1.20% week-on-week. The Capesize market remained weak, as the Hay Point-Qingdao route index posted consecutive declines over the week, falling 4.42% week-on-week.

Tianjin Bulk Grain Freight Index (TBGI) Closed at 930.63 points, up 4.25 points (0.46%) compared to Aug.15 (the last release day of Week 33). Stronger grain shipments from South America supported firm market rates, with the South America-Tianjin route index rising 0.42% week-on-week. The US Gulf-Tianjin and US West Coast-Tianjin route indices also strengthened, up 0.55% and 0.17% week-on-week, respectively.

Tianjin Bulk Mineral Freight Index (TBMI) Closed at 1502.02 points, down 86.25 points (5.43%) compared to Aug. 15 (the last release day of Week 33). In the iron ore market, growing caution and weaker transport demand drove rates lower, with the West Australia-Northern China route index falling 7.20% week-on-week and the Brazil-Tianjin route index down 3.64%. The nickel ore market saw support from firmer Supramax vessel rates, pushing the Surigao-Tianjin route index up 2.70% week-on-week.

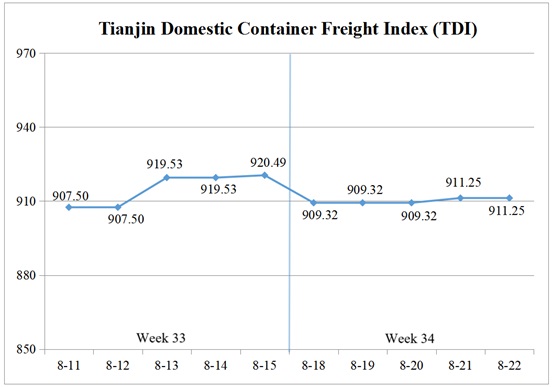

IV. Tianjin Domestic Container Freight Index (TDI)

In Week 34, 2025 (Aug.18-Aug.22), the trend of the Tianjin Domestic Container Freight Index (TDI) is shown in the chart below:

In Week 34, the Tianjin Domestic Container Freight Index experienced a slight decline.

The outbound index remained stable during the week, while the inbound index dropped significantly on Aug.18 (Mon.) and saw a minor recovery on Aug.21 (Thur.). Affected by the fluctuations in the inbound index, the TDI declined at the beginning of the week and edged up slightly in the latter part. It closed at 911.25 points on Aug.22 (Fri.), a cumulative decline of 9.24 points or 1.00% compared to Aug.15 (the last release day of Week 33).

The TDI index value and several ups and downs on a day-on-day basis are as follows:

The Tianjin Domestic Container Outward Freight Index (TDOI) Remained stable, closing at 963.78 points on Aug.22, unchanged from Aug.15 (the last release day of Week 33). To ensure order delivery, shippers accelerated shipments. However, booking demand during the off-season was still insufficient compared to shipping capacity supply, so the market freight rates remained stable. The freight indices for the routes from Tianjin to Guangzhou, Tianjin to Quanzhou/Xiamen, and Tianjin to Shanghai closed at 918.81 points, 1116.47 points, and 1110.30 points, respectively, all unchanged week-on-week.

The Tianjin Domestic Container Inward Freight Index (TDII) Declined noticeably, closing at 858.72 points on Aug.22, with a cumulative decline of 18.48 points or 2.11% compared to Aug.15 (the last release day of Week 33). Booking demand in South China remained stable, and freight rates for the Guangzhou to Tianjin route continued the rising trend, with the index closing at 929.29 points, up 3.42% week-on-week. In Fujian market, weaker cargo volume support led to a significant decline in freight rates for the Quanzhou/Xiamen to Tianjin route, with the index closing at 463.85 points, hitting the lowest level since the beginning of the year, down 32.72% week-on-week. Freight rates in East China remained stable, with the index for the Shanghai to Tianjin route closing at 1061.42 points, unchanged week-on-week.

(The analysis report is for reference only and at your own risk)