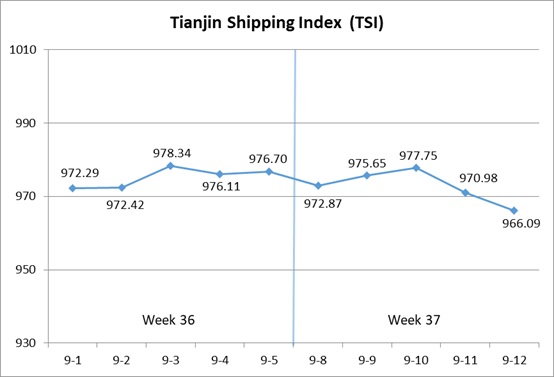

I. Tianjin Shipping Index (TSI)

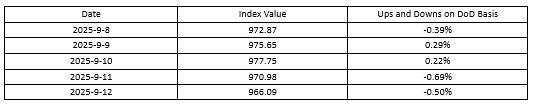

In Week 37, 2025 (Sep.8 to Sep.12), Tianjin Container Freight Index (TCI) continued to decrease. Tianjin Bulk Freight Index (TBI) rebounded slightly. Tianjin Domestic Container Freight Index (TDI) decreased. The TSI fluctuated downwards, eventually closing at 966.09 points, with a cumulative decrease of 10.61 points or 1.09% from Sep.5 (the last release day of Week 36). The trend of TSI is as follows:

The value and trend of TSI is as follows:

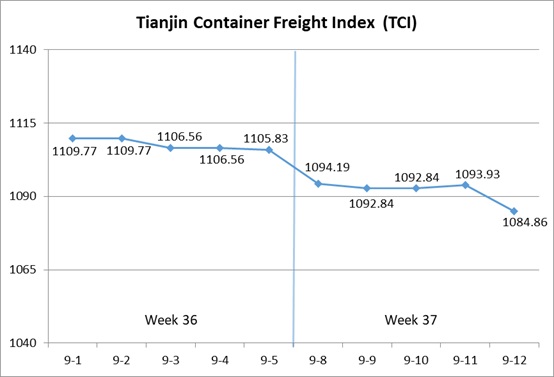

II. Tianjin Container Freight Index (TCI)

In Week 37, 2025 (Sep.8 to Sep.12), the trend of Tianjin Container Freight Index (TCI) is as follows:

In Week 37, the TCI continued to decrease.

From Sep.8-Sep.9 (Mon.-Tue.), the freight rates in European route, Mediterranean route, American East Coast route, South American West route and Central and South American route decreased, and the freight rate in American West Coast route increased at first and then decreased. The freight rates in South American East route, Indonesian route and Thailand-Vietnam route increased slightly. The TCI showed weakness, with a cumulative decrease of 1.17% on two releasing days. From Sep.10-Sep.12 (Wed.-Fri.), the freight rates in European route, Mediterranean route, American route, South American West route and South American East route decreased, and the freight rate in Indonesian route continued to increase. The freight rates in Central and South American route and Thailand-Vietnam route kept steady. The TCI decreased, with a cumulative decrease of 0.73% on three releasing days.

Finally, the TCI closed at 1084.86 points, with a cumulative decrease of 20.97 points (1.90%) from Sep.5 (the last release day of Week 36).

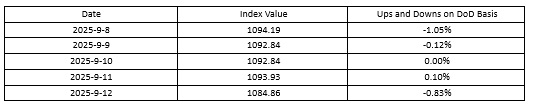

The TCI index value and several ups and downs on a day-on-day basis are as follows:

The TCI includes 19 sample routes. The main route analysis of this week is as follows:

European/Mediterranean route The market supply was limited, and shipping companies were encouraging the carriage of high-cube light cargo. As a result, market freight rates further decreased. The freight indices in European route, Mediterranean East route and Mediterranean West route closed at 668 points, 842.99 points and 1121.58 points, with the decrease of 7.76%, 4.27% and 3.56% on a week-on-week basis.

American route Before the National Day holiday, market shipments fell short of expectations, prompting shipping companies to announce plans for suspension of voyage services around the holiday. This week the freight rate for American West Coast route surged and then fell, with the freight rate index closing at 842.13 points, with the increase of 1.76% on a week-on-week basis. The American East Coast route experienced a smaller suspension, with the freight rate declining this week, and the freight rate index closing at 817.62 points, with the decrease of 3.30% on a week-on-week basis.

South American route Freight rates showed divergent trends. On the South American West route, the market cargo volume struggled to support high freight rates, leading to a rapid decline this week. The freight rate index closed at 1072.42 points, with the decrease of 9.45% on a week-on-week basis. On the South American East route, heavy cargo space became tight, prompting some shipping companies to increase the General Rate Increase (GRI). The freight rate index closed at 1525.89 points, with the increase of 2.50% on a week-on-week basis. On the Central and South American route, both supply and demand in the transportation market were weak. Some shipping companies slightly reduced freight rates to attract cargo, with the freight rate index closing at 1289.90 points, with the decrease of 0.20% on a week-on-week basis.

Southeast Asian route Before the National Day holiday, shippers concentrated on cargo shipments, leading to a tightening of spot shipping space and a slight increase in market freight rates. The freight rate indices for the Tianjin-Indonesia route and the Tianjin-Thailand-Vietnam route closed at 464.44 and 383.45 points respectively, with the increase of 1.34% and 0.71% on a week-on-week basis.

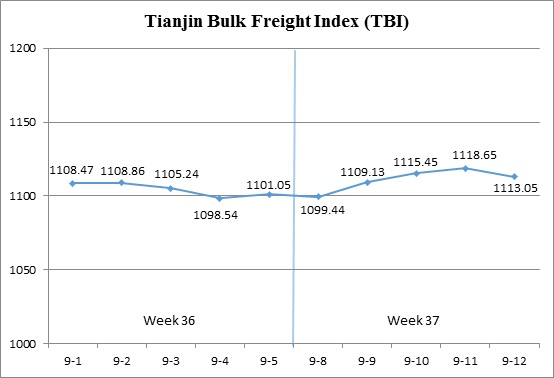

III. Tianjin Bulk Freight Index (TBI)

In Week 37, 2025 (Sept.8 to Sept.12), the trend of Tianjin Bulk Freight Index (TBI) was released as follows:

In Week 37, the TBI rebounded slightly.

On Sept.8 (Mon.), freight rates in the grain market edged higher while coal and metal ore rates saw slight declines, leading the TBI to dip by 0.15% on the day. Subsequently, freight rates in the coal market posted a modest rebound, freight rates in the grain market continued to strengthen, and freight rates in the metal ore market rose sharply, leading the TBI to climb for three consecutive sessions from Sept.9 to 11 (Tue. to Thur.), with a cumulative increase of 1.75%. On Sept.12 (Fri.), freight rates in the coal and metal ore market retreated, pulling the TBI slightly lower. The index ultimately closed at 1113.05 points, up 12.00 points or 1.09% compared to Sept.5 (the last release day of Week 36).

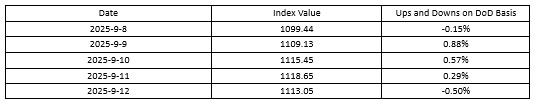

The TBI index value and several ups and downs on a day-on-day basis are as follows:

Tianjin Bulk Coal Freight Index (TBCI)Closed at 825.92 points, up 6.57 points or 0.80% compared to Sept.5 (the last release day of Week 36). In the supramax segment, limited Indonesian coal cargo availability weighed on rates, with the Indonesia-Qingdao route index declining 0.78% week-on-week. The capesize market showed steady gains, as the Hay Point-Qingdao route index rose 1.81% over the week.

Tianjin Bulk Grain Freight Index (TBGI) Closed at 952.08 points, an increase of 10.82 points or 1.15% compared to Sept.5 (the last release day of Week 36). Continued release of South American grain cargoes absorbed part of the panamax vessel capacity, supporting a rebound in market rates. The South America-Tianjin route index rose 1.03% week-on-week, while the U.S. Gulf-Tianjin and U.S. West Coast-Tianjin route indices increased by 1.33% and 0.68%, respectively.

Tianjin Bulk Mineral Freight Index (TBMI) Closed at 1561.16 points, up 18.63 points or 1.21% from Sept.5 (the last release day of Week 36). In the iron ore market, strong chartering activity by Australian miners early in the week drove a notable rise in freight rates. However, with FFA forward contract prices declining later in the week, market sentiment weakened. The Australia West-North China route index rose 1.67% week-on-week, while weaker cargo demand from Brazil saw the Brazil-Tianjin route index edge up only 0.09%. In the nickel ore market, accelerated shipments from the Philippines provided additional support, with the Surigao-Tianjin route index climbing 0.43% week-on-week.

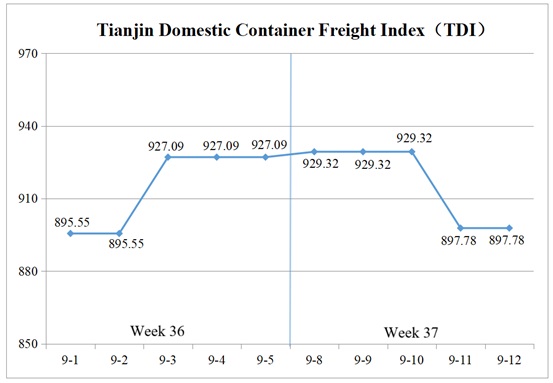

IV. Tianjin Domestic Container Freight Index (TDI)

In Week 37 (Sep.8 to Sep.12), the trend of the Tianjin Domestic Container Freight Index (TDI) is shown in the chart below:

In Week 37, the Tianjin Domestic Container Freight Index declined noticeably.

On Sep.8 (Mon.), the inbound index rose slightly, driving a modest increase in TDI, which remained stable from Sep.9 to 10 (Tue. to Wed.). On Sep.11 (Thur.), both the inbound and outbound indices fell sharply, pushing TDI back to the level seen at the start of the previous week. On Sep.12 (Fri.), TDI stabilized and closed at 897.78 points, a cumulative decrease of 29.31 points or 3.16% compared to Sep.5 (the last release day of Week 36).

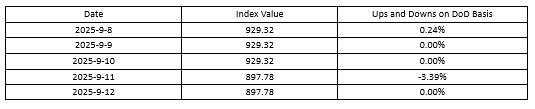

The TDI index value and several ups and downs on a day-on-day basis are as follows:

The Tianjin Domestic Container Outward Freight Index (TDOI) Declined sharply and closed at 933.44 points on Sep.12, a cumulative decrease of 24.05 points or 2.51% compared to Sep.5 (the last release day of Week 36). In the Tianjin outbound domestic container market, shipment volumes increased while shipping space supply gradually expanded, leading to a decline in freight rates. The freight indices for the Tianjin to Guangzhou route, Tianjin to Quanzhou/Xiamen route, and Tianjin to Shanghai route closed at 888.32 points, 1085.51 points, and 1082.57 points, respectively, down by 2.39%, 2.88%, and 2.79% week-on-week.

The Tianjin Domestic Container Inward Freight Index (TDII) Fluctuated downward and closed at 862.12 points on Sep.12, a cumulative decrease of 34.57 points or 3.86% compared to Sep.5 (the last release day of Week 36). Typhoons had a temporary impact on hub ports in South China, causing congestion at some inland barge terminals. Meanwhile, shipping volumes in the Fujian and East China markets remained insufficient, resulting in obvious declines in freight rates across various routes. The freight indices for the Guangzhou to Tianjin, Quanzhou/Xiamen to Tianjin, and Shanghai to Tianjin routes closed at 929.29 points, 482.71 points, and 1061.42 points respectively, with week-on-week decreases of 3.74%, 3.72%, and 4.70%.

(The analysis report is for reference only and at your own risk)