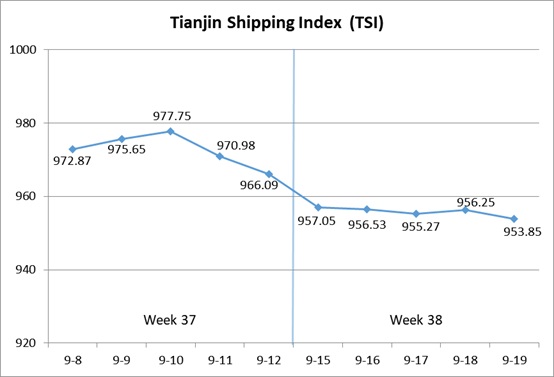

I. Tianjin Shipping Index (TSI)

In Week 38, 2025 (Sep.15 to Sep.19), Tianjin Container Freight Index (TCI) continued to decrease. Tianjin Bulk Freight Index (TBI) fluctuated upwards. Tianjin Domestic Container Freight Index (TDI) increased steadily. The TSI decreased slowly, eventually closing at 953.85 points, with a cumulative decrease of 12.24 points or 1.27% from Sep.12 (the last release day of Week 37). The trend of TSI is as follows:

The value and trend of TSI is as follows:

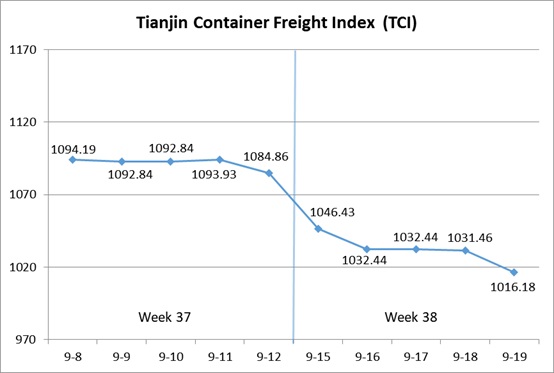

II. Tianjin Container Freight Index (TCI)

In Week 38, 2025 (Sep.15 to Sep.19), the trend of Tianjin Container Freight Index (TCI) is as follows:

In Week 38, the TCI continued to decrease.

From Sep.15-Sep.16 (Mon.-Tue.), the freight rates in European route, Mediterranean route, South American route and Indian route decreased rapidly, and the freight rate in American West Coast route increased at first and then decreased. The freight rate in American East Coast route continued to increase slightly. The TCI decreased significantly, with a cumulative decrease of 4.83% on two releasing days. From Sep.17-Sep.19 (Wed.-Fri.), the freight rates in European route, Mediterranean route, American West Coast route, South American route and Indian route continued to decrease, and the freight rate in American East Coast route decreased steadily. The TCI decreased, with a cumulative decrease of 1.57% on three releasing days.

Finally, the TCI closed at 1016.18 points, with a cumulative decrease of 68.68 points (6.33%) from Sep.12 (the last release day of Week 37).

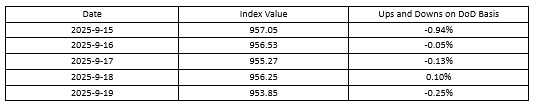

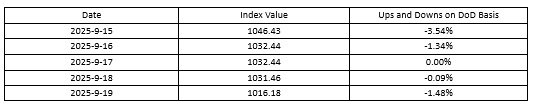

The TCI index value and several ups and downs on a day-on-day basis are as follows:

The TCI includes 19 sample routes. The main route analysis of this week is as follows:

European/Mediterranean route Due to the sluggish market demand, shipping companies reduced their capacity supply, leading to a significant decline in freight rates. The freight indices in European route, Mediterranean East route and Mediterranean West route closed at 538.10 points, 785.48 points and 977.32 points, with the decrease of 19.45%, 6.82% and 12.86% on a week-on-week basis.

American route Freight rates saw mixed performance. For the American West Coast route, shipping companies had been securing cargo sources for voyages around the National Day holiday. After a brief rebound at the beginning of the week, the freight rate turned down, with the freight rate index closing at 832.50 points, with the decrease of 1.14% on a week-on-week basis. For the American East Coast route, some shippers concentrated their shipments before the holiday, coupled with significant suspension efforts by shipping companies, resulting in tight spot space for some voyages, which drove the freight rate to fluctuate and rise. The freight rate index closed at 826.73 points, with the increase of 1.11% on a week-on-week basis.

South American route Factory shipments decreased, coupled with shipping companies on the South American West route offering special rates to attract cargo, and the South American East route encouraging the carriage of heavy cargo. The imposition of tariffs on Mexico in the Central and South American route dragged down market expectations. This week the freight indices in South American West route, South American East route and Central and South American route closed at 792.56 points, 1445.52 points and 1210.59 points, with cumulative decrease of 26.10%, 5.27% and 6.15% during the week.

Indian route Recently the market demand for freight transportation had been sluggish, coupled with the entry of new ships into market operations, freight rates decreased significantly this week. The freight rate index closed at 825.56 points, with the decrease of 7.36% on a week-on-week basis.

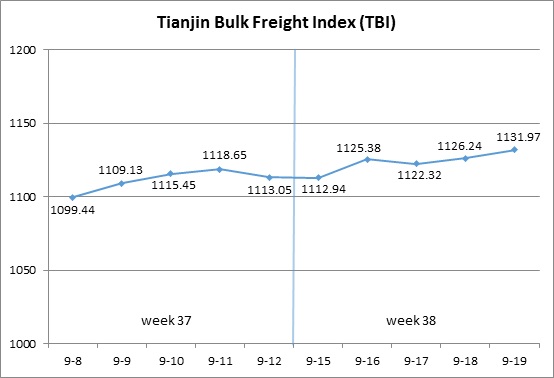

III. Tianjin Bulk Freight Index (TBI)

In Week 38, 2025 (Sep.15 to Sep.19), the trend of Tianjin Bulk Freight Index (TBI) was released as shown as follows:

In Week 38, the TBI rebounded slightly.

From Sep.15 to Sep.17 (Mon. to Wed.), coal market freight rates continued to rise slightly, grain market freight rates continued to weaken, metal ore market freight rates fluctuated and rose, and TBI showed a fluctuating upward trend, with a cumulative increase of 0.83% in the three release days. Subsequently, the grain market freight rates further declined, the coal market freight rates continued to rise, and the metal ore market freight rates also continued to rise, driving TBI to continue to rise from Sep.18 to Sep.19 (Thur. to Fri.) and ultimately closing at 1131.97 points, with a cumulative increase of 18.92 points or 1.70% compared with Sep.12 (the last release day of Week 37).

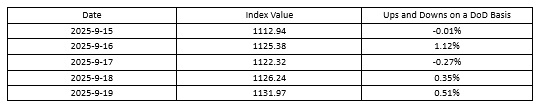

The TBI index value and several ups and downs on a day-on-day basis are as follows:

Tianjin Bulk Coal Freight Index (TBCI) Closed at 847.23 points, a cumulative increase of 21.31 points or 2.58% compared to Sep.12 (the last release day of Week 37). In terms of supramax market, there was no improvement in Indonesian coal cargo pallets, but the market capacity supply was slightly tight. The freight index for the Indonesia to Qingdao route increased by 1.27% week on week. The overall market freight rates for Capsize rose, with the freight index for the Hay Point to Qingdao route increasing by 3.39% on a weekly basis.

Tianjin Bulk Grain Freight Index (TBGI) Closed at 946.97 points, a cumulative decrease of 5.11 points or 0.54% compared to Sep.12 (the last release day of Week 37). The demand for grain transportation was weak, and market freight rates fell. The freight index for the South American to Tianjin route decreased by 0.82% on a weekly basis, the freight index for the US Gulf to Tianjin route decreased by 0.41% on a weekly basis, and the freight index for West American to Tianjin route decreased by 0.20% on a weekly basis.

Tianjin Bulk Mineral Freight Index (TBMI) Closed at 1601.71 points, a cumulative increase of 40.55 points or 2.60% compared to Sep.12 (the last release day of Week 37). In terms of iron ore, Australian miners inquired actively and coupled with the rise in FFA forward contract prices, the market atmosphere was gradually strengthening. The freight index for the Western Australia to Northern China route increased by 3.43% on a weekly basis. The trading volume of iron ore pallets in Brazil was limited, but driven by the positive trend in the Pacific market, the freight index for the Brazil to Tianjin route also increased by 1.29% on a weekly basis. In terms of nickel ore, the Philippine nickel ore inventory was still acceptable, and the freight index of the Surigao to Tianjin route was basically stable, with a slight decrease of 0.19% on a weekly basis.

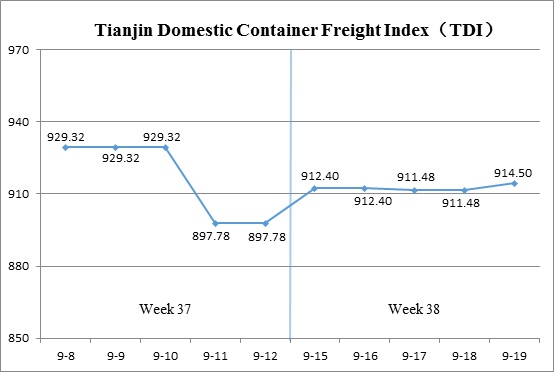

IV. Tianjin Domestic Container Freight Index (TDI)

In Week 38 (Sept.15 to Sept.19), the trend of the Tianjin Domestic Container Freight Index (TDI) is shown in the chart below:

In Week 38, the Tianjin Domestic Container Freight Index rebounded with fluctuations.

On Sept.15 (Mon.), the inbound index edged down slightly while the outbound index recovered, pushing the TDI marginally higher. From Sept.16 to 19 (Tue. to Fri.), the inbound index saw a sharper decline, but the outbound index continued its upward momentum, driving the TDI to oscillate higher. The index ultimately closed at 914.50 points, an increase of 16.72 points or 1.86% compared to Sept.12 (the last release day of Week 37).

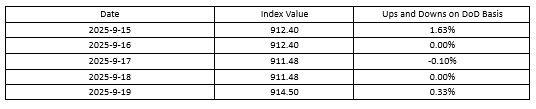

The TDI index value and several ups and downs on a day-on-day basis are as follows:

The Tianjin Domestic Container Outward Freight Index (TDOI) Rebounded, closing at 995.14 points on Sept.19, up 61.70 points or 6.61% compared with Sept.12 (the last release day of Week 37). In Tianjin’s outbound domestic container market, cargo volumes continued to grow, driving rates higher on routes to South China and Fujian. The Tianjin-Guangzhou and Tianjin-Quanzhou/Xiamen route indices closed at 962.87 points and 1125.71 points, representing week-on-week increases of 8.39% and 3.70%, respectively. Rates on routes to East China softened, with the Tianjin-Shanghai route index closing at 1060.93 points, down 2.00% week-on-week. Looking ahead, the market will enter a period of concentrated shipments ahead of the National Day holiday and mid-holiday replenishment demand. However, recent typhoon activity in the south may cause vessel schedule delays, potentially weakening the stability of capacity supply.

The Tianjin Domestic Container Inward Freight Index (TDII) Extended its decline, closing at 833.85 points on Sept. 19, down 28.27 points or 3.28% compared with Sept.12 (the last release day of Week 37). Typhoon disruptions in South China and Fujian led to congestion at certain barge terminals, delaying shippers’ deliveries and pushing rates further down. The Guangzhou-Tianjin and Quanzhou/Xiamen-Tianjin route indices closed at 896.23 points and 457.90 points, representing week-on-week decreases of 3.56% and 5.14%, respectively. The Shanghai-Tianjin route index remained stable at 1061.42 points, unchanged from the previous week.

(The analysis report is for reference only and at your own risk)