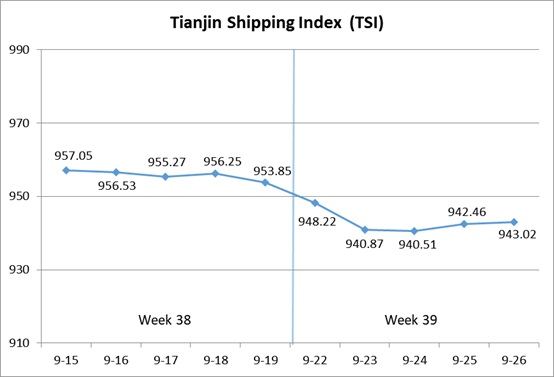

I. Tianjin Shipping Index (TSI)

In Week 39, 2025 (Sep.22 to Sep.26), Tianjin Container Freight Index (TCI) continued to decrease. Tianjin Bulk Freight Index (TBI) fluctuated in a narrow range. Tianjin Domestic Container Freight Index (TDI) climbed steadily. The TSI decreased rapidly and then kept steady, eventually closing at 943.02 points, with a cumulative decrease of 10.83 points or 1.14% from Sep.19 (the last release day of Week 38). The trend of TSI is as follows:

The value and trend of TSI is as follows:

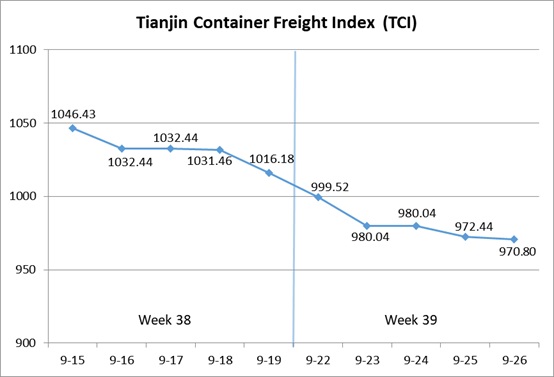

II. Tianjin Container Freight Index (TCI)

In Week 39, 2025 (Sep.22 to Sep.26), the trend of Tianjin Container Freight Index (TCI) is as follows:

In Week 39, the TCI continued to decrease.

From Sep.22-Sep.23 (Mon.-Tue.), the freight rates in European route, Mediterranean route, American route, South American route and Indian route decreased significantly. The TCI decreased rapidly, and the index value fell below the 1000-point mark, with a cumulative decrease of 3.56% on two releasing days. From Sep.24-Sep.26 (Wed.-Fri.), the freight rates in European route, Mediterranean route, American route and Indian route decreased steadily, and the freight rate in South American route kept steady. The TCI’s decline narrowed, with a cumulative decrease of 0.94% on three releasing days.

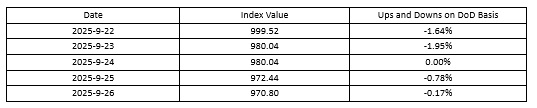

Finally, the TCI closed at 970.80 points, with a cumulative decrease of 45.38 points (4.47%) from Sep.19 (the last release day of Week 38). The TCI index value and several ups and downs on a day-on-day basis are as follows:

The TCI includes 19 sample routes. The main route analysis of this week is as follows:

European/Mediterranean route As the long holiday approached, the demand for booking space continued to shrink. Shipping companies launched special pricing for space and measures such as waiving overweight fees for small containers to increase their efforts to attract cargo. Market freight rates further decreased. The freight indices in European route, Mediterranean East route and Mediterranean West route closed at 507.13 points, 751.40 points and 912.41 points, with the decrease of 5.76%, 4.34% and 6.64% on a week-on-week basis.

American route At the beginning of the week, the market volume was sluggish, and some shipping companies significantly reduced prices to increase the loading rate. As various shipping alliances gradually implemented the suspension plan, the decline in market freight rates slowed down in the middle and later parts of the week. The freight indices in American West Coast route and American East Coast route closed at 744.78 points and 759.75 points, with the cumulative decrease of 10.54% and 8.10% respectively during the week.

South American route The spot market was abundant, with fierce competition in cargo supply. Shipping companies continued to reduce freight rates. The freight indices in South American West route, South American East route and Central and South American route closed at 702.56 points, 1341.64 points and 1149.52 points, with the cumulative decrease of 11.36%, 7.19% and 5.04% during the week.

Indian route The US-India tariff negotiations affected market expectations. Indian purchasing companies slowed down their demand for imported raw materials to reduce trade risks. Coupled with the recent increase in direct shipping to India by shipping companies, market freight rates accelerated their decline. The freight rate index closed at 702.66 points this week, with the decrease of 14.89% on a week-on-week basis.

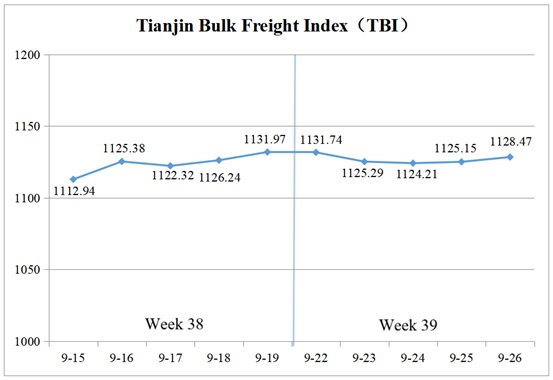

III. Tianjin Bulk Freight Index (TBI)

In Week 39, 2025 (Sep.22 to Sep.26), the trend of Tianjin Bulk Freight Index (TBI) was released as shown as follows:

In Week 39, the TBI fluctuated within a narrow range.

From Sep.22 to Sep.24 (Mon. to Wed.), the coal and grain market freight rates continued to decline slightly, while the metal ore market freight rates trended lower, leading to slight decreases for the TBI in three consecutive releasing days, with a cumulative drop of 0.69%. Subsequently, the coal and grain markets freight rates gradually stabilized, and the metal ore market freight rates saw a slight rebound, driving the TBI to recover slightly from Sep.25 to Sep.26 (Thur. to Fri.). The TBI finally closed at 1128.47 points, with a cumulative decrease of 3.50 points or 0.31% compared to Sep.19 (the last release day of Week 38).

The TBI index value and several ups and downs on a day-on-day basis are as follows:

Tianjin Bulk Coal Freight Index (TBCI) Closed at 836.53 points, a cumulative decrease of 10.70 points or 1.26% compared to Sep.19 (the last release day of Week 38). In terms of Supramax market, coal cargoes volumes from Indonesia further decreased, while the spot shipping capacity supply increased. The freight index for the Indonesia to Qingdao route fell by 1.68% week-on-week. In the Capesize market, the freight index for the Hay Point to Qingdao route declined, declining by 1.01% on a weekly basis.

Tianjin Bulk Grain Freight Index (TBGI) Closed at 944.74 points, a cumulative decrease of 2.23 points or 0.24% compared to Sep.19 (the last release day of Week 38). The demand for grain transportation from South America remained weak, and the available shipping capacity in the Atlantic market increased. The freight index for the South American to Tianjin route dropped by 0.35% week-on-week, and that for the US Gulf to Tianjin route fell by 0.31% week-on-week. In contrast, typhoon weather affected the turnover of ships, making the shipping capacity in the Pacific market slightly tight, and the freight index for the West American to Tianjin route rose by 0.47% week-on-week.

Tianjin Bulk Mineral Freight Index (TBMI) Closed at 1604.15 points, a cumulative increase of 2.44 points or 0.15% compared to Sep.19 (the last release day of Week 38). In terms of iron ore, the Pacific market was relatively quiet at the beginning of the week, and the freight rate for the Western Australia to Northern China route declined from a high level. In the latter part of the week, Australian miners were active in inquiring about cargoes, and the market sentiment improved. The freight rate for the Western Australia to Northern China route rebounded slightly, with the route’s freight index falling by 0.56% week-on-week. The number of iron ore cargo orders in Brazil increased, and the freight index for the Brazil to Tianjin route rose continuously during the week, with a 3.13% week-on-week increase. In terms of nickel ore, the market had sufficient shipping capacity supply, and the freight index for the Surigao to Tianjin route decreased by 0.96% on a weekly basis.

IV. Tianjin Domestic Container Freight Index (TDI)

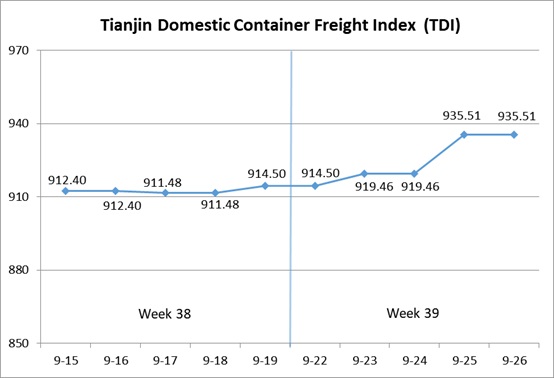

In Week 39 (Sept.22 to Sept.26), the trend of the Tianjin Domestic Container Freight Index (TDI) is shown in the chart below:

In Week 39, the Tianjin Domestic Container Freight Index increased significantly.

The outbound index remained stable this week, while the inbound index showed a slight increase on Sept.23 (Tue.), followed by a significant rise on Sept.25 (Thur.), driving up the TDI. On Sept.26 (Fri.), the TDI closed at 935.51 points, an increase of 21.01 points or 2.30% compared to Sept.19 (the last release day of Week 38).

The TDI index value and several ups and downs on a day-on-day basis are as follows:

The Tianjin Domestic Container Outward Freight Index (TDOI) Kept steady, closing at 995.14 points on Sept.26, unchanged compared with Sept.19 (the last release day of Week 38). With the National Day holiday approaching, outbound domestic container shipping volumes in Tianjin increased, leading to tighter pre-holiday and holiday available space. Market freight rates remained steady. The freight indices for Tianjin-Guangzhou, Tianjin-Quanzhou/Xiamen, and Tianjin-Shanghai routes closed at 962.87 points, 1125.71 points, and 1060.93 points respectively, showing no week-on-week change.

The Tianjin Domestic Container Inward Freight Index (TDII) Stopped falling and rebounded, closing at 875.88 points on Sept. 26, up 42.03 points or 5.04% compared with Sept.19 (the last release day of Week 38). The impact of Typhoon Ragasa on operations at southern coastal ports and vessel schedules had tightened capacity supply, causing market freight rates to stop declining and rise instead. The freight indices for Guangzhou-Tianjin and Quanzhou/Xiamen-Tianjin routes closed at 929.29 points and 559.19 points respectively, up 3.69% and 22.12% week-on-week. Meanwhile, the Shanghai-Tianjin route remained stable, with its freight index closing at 1061.42 points, unchanged from the previous week.

(The analysis report is for reference only and at your own risk)