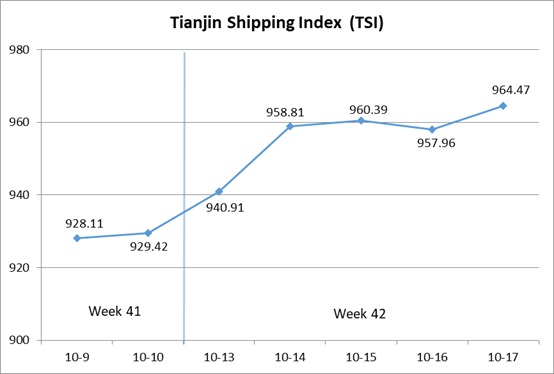

I. Tianjin Shipping Index (TSI)

In Week 42, 2025 (Oct.13 to Oct.17), Tianjin Container Freight Index (TCI) increased at first and then decreased. Tianjin Bulk Freight Index (TBI) fluctuated upwards. Tianjin Domestic Container Freight Index (TDI) increased significantly. The TSI climbed steadily, eventually closing at 964.47 points, with a cumulative increase of 35.05 points or 3.77% from Oct.10 (the last release day of Week 41). The trend of TSI is as follows:

The value and trend of TSI is as follows:

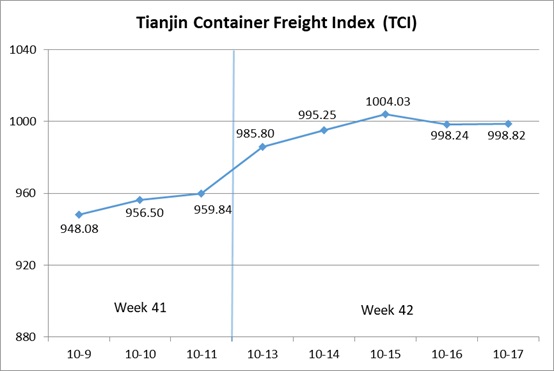

II. Tianjin Container Freight Index (TCI)

In Week 42, 2025 (Oct.13 to Oct.17), the trend of Tianjin Container Freight Index (TCI) is as follows:

In Week 42, the TCI rose sharply before slightly retreating.

From Oct.13-Oct.15 (Mon.-Wed.), the freight rates in European route, Mediterranean West route, American route, South American West route, South American East route, Indonesian route and Thailand-Vietnam route increased, and the freight rates in Mediterranean East route and Central and South American route increased at first and then decreased. The TCI climbed rapidly, with a cumulative increase of 4.60% on three releasing days. From Oct.16-Oct.17 (Thur.-Fri.), the freight rate in European route fluctuated downwards, and the freight rate in South American West route continued to increase. The freight rates in Indonesian route and Thailand-Vietnam route decreased slightly. The freight rates in Mediterranean route, American route, South American East route and Central and South American route kept steady. The TCI decreased, with a cumulative decrease of 0.52% on two releasing days.

Finally, the TCI closed at 998.82 points, with a cumulative increase of 38.98 points (4.06%) from Oct.11 (the last release day of Week 41).

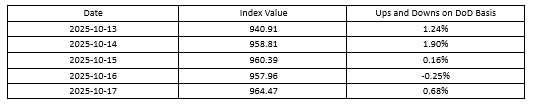

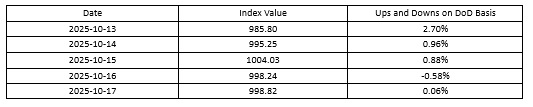

The TCI index value and several ups and downs on a day-on-day basis are as follows:

The TCI includes 19 sample routes. The main route analysis of this week is as follows:

European/Mediterranean route Freight rates showed divergent trends across regions. On the European route and the Mediterranean West route, post-holiday available capacity tightened significantly amid persistent port congestion at Rotterdam, Antwerp, and Genoa, prompting carriers to implement rate hikes and driving a strong rebound in freight rates. The freight indices closed at 590.29 points and 958.39 points, with the cumulative increase of 13.32% and 6.50%. In contrast, on the Mediterranean East route, weak factory shipments led shipping alliances to maintain discounted space offerings, resulting in a slight rate decline. The freight index closed at 747.95 points, with the cumulative decrease of 0.70% on a week-on-week basis.

American route Frequent adjustments to local tariff policies and port regulations, coupled with reduced sailings and capacity cuts by shipping lines, drove a strong rebound in freight rates this week. The freight indices in American West Coast route and American East Coast route closed at 775.41 points and 782.59 points, with the cumulative increase of 5.23% and 4.25%.

South American route Freight rates showed divergent trends. On the South American West route and the South American East route, shipping companies reduced the number of voyages, and light cargo space remained tight. Coupled with Mexico’s strengthened customs inspection policy, ship berthing delays occurred. This week freight rates climbed significantly. The freight indices closed at 907.79 points and 1451.49 points, with the cumulative increase of 15.54% and 20.90%. In contrast, on the Central and South American route, post-holiday capacity was abundant, and the freight rate fluctuated downwards. The freight index closed at 1073.64 points, with the cumulative decrease of 1.11%.

Southeast Asian route Market cargo volume rebounded, with typhoons causing liner delays and tight spot space. The freight indices in Indonesian route and Thailand-Vietnam route closed at 501.36 points and 386.16 points, with the increase of 3.49% and 1.42% on a week-on-week basis.

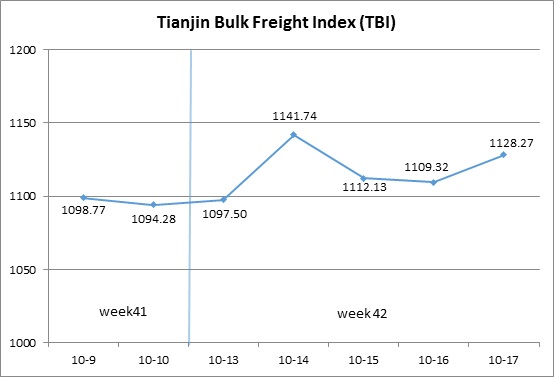

III. Tianjin Bulk Freight Index (TBI)

In Week 42, 2025 (Oct.13 to Oct.17), the trend of Tianjin Bulk Freight Index (TBI) was released as shown as follows:

In Week 42, the TBI fluctuated.

From Oct.13 to Oct.14 (Mon. to Tue.), coal and grain market freight rates continued to rise slightly, while metal ore market freight rates quickly climbed, driving TBI to rebound continuously, with a cumulative increase of 4.34% over the two release days. Subsequently, coal and grain market freight rates fluctuated narrowly, while metal ore market freight rates experienced a decline. TBI fell by 2.84% from Oct.15 to Oct.16 (Wed. to Thur.). On Oct.17 (Fri.), the coal and metal ore market saw a slight increase in freight rates, driving TBI to stabilize and rebound, ultimately closing at 1128.27 points, with a cumulative increase of 33.99 points or 3.01% compared to Oct.10 (the last release day of Week 41).

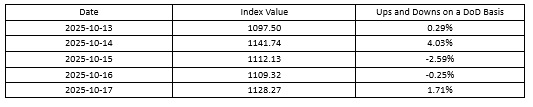

The TBI index value and several ups and downs on a day-on-day basis are as follows:

Tianjin Bulk Coal Freight Index (TBCI) Closed at 851.12 points, a cumulative increase of 28.22 points or 3.43% compared to Oct.10 (the last release day of Week 41). In terms of the supramax market, there was a slight increase in Indonesian coal shipments, and the freight index for the Indonesia to Qingdao route increased moderately, with a cumulative increase of 0.73% this week. In terms of the Capsize market, the freight index of the Hay Point to Qingdao route fluctuated significantly with the overall market, rising 5.08% on a weekly basis.

Tianjin Bulk Grain Freight Index (TBGI) Closed at 942.30 points, a cumulative increase of 1.61 points or 0.17% compared to Oct.10 (the last release day of Week 41). Due to policy reasons, the available transportation capacity in the market was tight, and freight rates increased slightly. The freight index for the US Gulf to Tianjin route increased by 0.31% on a weekly basis, while the freight index for the West America to Tianjin route increased by 0.33% on a weekly basis. In contrast, the supply and demand of transportation capacity in South America were basically balanced, and the freight index for the South America to Tianjin route fell by 0.08% on a weekly basis.

Tianjin Bulk Mineral Freight Index (TBMI) Closed at 1591.38 points, a cumulative increase of 72.12 points or 4.75% compared to Oct.10 (the last release day of Week 41). In terms of iron ore, the FFA forward contract freight rate rose at the beginning of the week, which increased the willingness of ship owners to raise prices and led to a significant increase in market freight rates. Subsequently, due to the lack of transportation demand support, market sentiment cooled down, and freight rates fell. The freight index for the Western Australia to Northern China route increased by 6.49% on a weekly basis, while the freight index for the Brazil to Tianjin route increased by 1.47% on a weekly basis. In terms of nickel ore, the freight index for the Surigao to Tianjin route increased by 0.21% on a weekly basis.

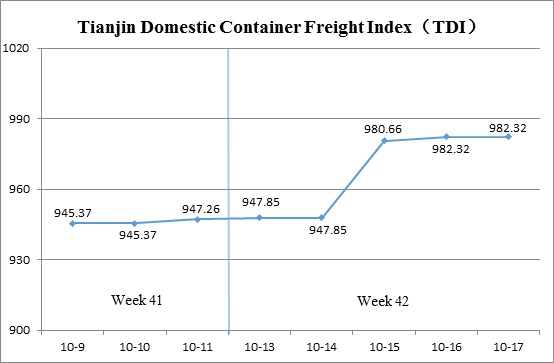

IV. Tianjin Domestic Container Freight Index (TDI)

In Week 42 (Oct.13 to Oct.17), the trend of the Tianjin Domestic Container Freight Index (TDI) is shown in the chart below:

In Week 42, the Tianjin Domestic Container Freight Index saw an expanded upward trend.

From Oct.13 to 14 (Mon. to Tue.), the inbound index rose slightly, with the TDI showing a modest increase. Between Oct. 15 and 17 (Wed.), the outbound index also saw a small gain, while the inbound index continued to strengthen, driving the TDI higher. The index ultimately closed at 982.32 points, up 35.06 points, or 3.70%, compared to Oct.11 (the last release day of Week 41).

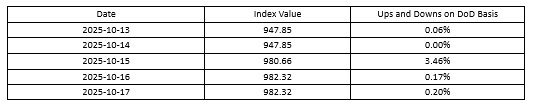

The TDI index value and several ups and downs on a day-on-day basis are as follows:

The Tianjin Domestic Container Outward Freight Index (TDOI) Continued its upward trend, closing at 1,028.27 points on Oct.17, marking a 29.34-point increase, or 2.94%, compared to Oct.11 (the last release day of Week 41). In the Tianjin outbound domestic container market, cargo volumes saw a slight increase, with freight rates rising towards Fujian and South China. The Tianjin-Quanzhou/Xiamen and Tianjin-Guangzhou route indices reached 1,211.79 points and 989.13 points, respectively, reflecting cumulative increases of 5.28% and 2.73%. Freight rates on the Tianjin–Shanghai route remained stable, with the index holding steady at 1,060.93 points for the week.

The Tianjin Domestic Container Inward Freight Index (TDII) Continued its upward trajectory, reaching 936.36 points on Oct.17, a cumulative increase of 40.77 points or 4.55% compared to Oct.11 (the last release day of Week 41). With weather conditions gradually improving, port congestion eased, and market capacity began to recover. Cargo volumes in South China and Fujian increased, driving freight rates higher. The Quanzhou/Xiamen–Tianjin and Guangzhou–Tianjin route indices rose to 761.54 points and 962.70 points, reflecting cumulative increases of 13.88% and 3.60%, respectively. Freight rates on the Shanghai–Tianjin route remained stable, with the index holding steady at 1,061.42 points for the week.

(The analysis report is for reference only and at your own risk)