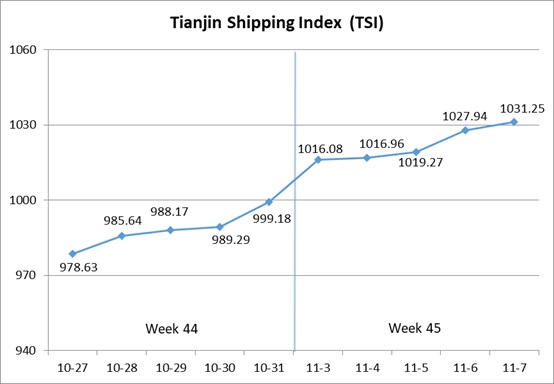

I. Tianjin Shipping Index (TSI)

In Week 45, 2025 (Nov.3 to Nov.7), Tianjin Container Freight Index (TCI) continued to increase. Tianjin Bulk Freight Index (TBI) stopped falling and rebounded. Tianjin Domestic Container Freight Index (TDI) increased steadily. The TSI climbed steadily, eventually closing at 1031.25 points, with a cumulative increase of 32.07 points or 3.21% from Oct.31 (the last release day of Week 44). The trend of TSI is as follows:

The value and trend of TSI is as follows:

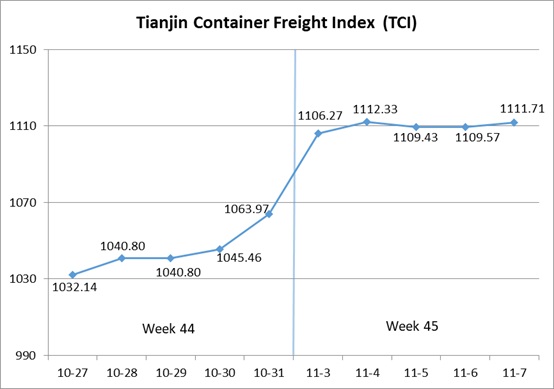

II. Tianjin Container Freight Index (TCI)

In Week 45, 2025 (Nov.3 to Nov.7), the trend of Tianjin Container Freight Index (TCI) is as follows:

In Week 45, the TCI saw further increase.

From Nov.3-Nov.4 (Mon.-Tue.), the freight rates in European route, Mediterranean route, American route, South American West route, Central and South American route and Persian Gulf route increased strongly, and the freight rate in South American East route increased at first and then decreased. The TCI increased significantly, with a cumulative increase of 4.55% on two releasing days. From Nov.5-Nov.7 (Wed.-Fri.), the freight rate in European route decreased slightly, and the freight rate in Mediterranean route increased steadily. The freight rate in American route decreased greatly, and the freight rates in South American route and Persian Gulf route kept steady. The TCI fluctuated downwards, with a cumulative decrease of 0.06% on three releasing days.

Finally, the TCI closed at 1111.71 points, with a cumulative increase of 47.74 points (4.49%) from Oct.31 (the last release day of Week 44).

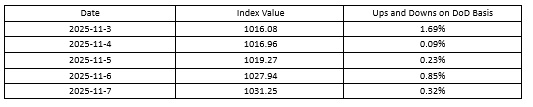

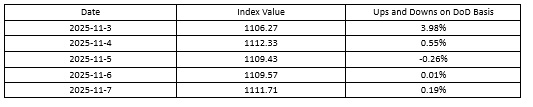

The TCI index value and several ups and downs on a day-on-day basis are as follows:

The TCI includes 19 sample routes. The main route analysis of this week is as follows:

European/Mediterranean route Market capacity remained at a low level, with more shipping companies joining the ranks of price hikes, and freight rates continued to rise at the beginning of the week. Subsequently, some shipping companies on European route introduced special-rate cabins, and the freight rate began to fall in the middle and later parts of the week. The freight index closed at 654.72 points, with the increase of 3.26% on a week-on-week basis. The freight rate on Mediterranean route showed a slight increase in stability in the middle and later parts of the week. The freight indices in Mediterranean East route and Mediterranean West route closed at 867.52 points and 1134.39 points, with the increase of 7.14% and 5.46% on a week-on-week basis.

American route The conclusion of a new phase of trade agreement between China and the United States boosted market expectations. At the beginning of the week, market freight rates continued to rise. However, in the middle and later parts of the week, shipping companies reduced freight rates to attract cargo, leading to a weakening of freight rates. The freight indices in American West Coast route and American East Coast route closed at 973.88 points and 909.87 points, with the cumulative increase of 3.77% and 1.18% in the week.

South American route Freight rates showed divergent trends. On the South American West route and Central and South American route, shipping companies continued to push up FAK, PSS, and GRI this week, with freight rates remaining relatively strong. The freight indices closed at 1011.25 points and 1035.90 points, with the increase of 8.76% and 6.94% on a week-on-week basis. On the South American East route, the market cargo volume struggled to support the current space supply, dragging down the freight rate to fluctuate and fall this week. The freight index closed at 1349.10 points, with the decrease of 0.67% on a week-on-week basis.

Persian Gulf route The market was experiencing tight spot capacity, with insufficient heavy cargo space. Shipping companies generally increased the freight rate, and the freight index closed at 947.30 points, with the increase of 15.90% on a week-on-week basis.

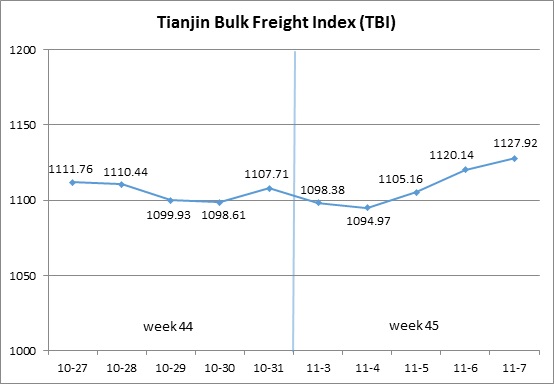

III. Tianjin Bulk Freight Index (TBI)

In Week 45, 2025 (Nov.3 to Nov.7), the trend of Tianjin Bulk Freight Index (TBI) was released as shown as follows:

In Week 45, the TBI showed weakness at the beginning of the week and continued to rebound in the later part of the week.

From Nov.3 to Nov.4 (Mon. to Tue.), the freight rates in the coal, grain, and metal ore markets slightly decreased, dragging down TBI’s continuous decline, with a cumulative drop of 1.15% over the two release days. From Nov.5 to Nov.7 (Wed. to Fri.), the grain market freight rates fluctuated narrowly, while the coal and metal ore market freight rates stabilized and rebounded, driving the TBI to rise continuously and ultimately closing at 1127.92 points, a cumulative increase of 20.21 points or 1.82% compared with Oct.31 (the last release day of Week 44).

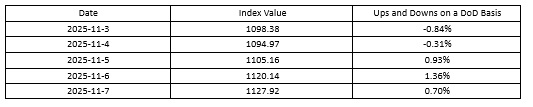

The TBI index value and several ups and downs on a day-on-day basis are as follows:

Tianjin Bulk Coal Freight Index (TBCI) Closed at 852.23 points, a cumulative increase of 11.79 points or 1.40% compared to Oct.31 (the last release day of Week 44). In terms of the supramax market, there was a shortage of coal cargo in Indonesia at the beginning of the week, and the freight index for the Indonesia to Qingdao route continued to be weak at the beginning of the week, but slightly stabilized in the later part of the week, with a cumulative decline of 0.15% this week. In terms of the Capsize market, Australian coal pallets increased in the later part of the week, and the freight index of the Hay Point to Qingdao route also fell first and then rose this week, with a week on week increase of 2.31%.

Tianjin Bulk Grain Freight Index (TBGI) Closed at 941.15 points, a cumulative decrease of 1.32 points or 0.14% compared to Oct.31 (the last release day of Week 44). The grain market freight rates continued to show a narrow wave trend, with the South American to Tianjin route freight index rising by 0.25% on a weekly basis, the US Gulf to Tianjin route freight index falling by 0.45% on a weekly basis, and the West America to Tianjin route freight index rising by 0.01% on a weekly basis.

Tianjin Bulk Mineral Freight Index (TBMI) Closed at 1590.39 points, a cumulative increase of 50.17 points or 3.26% compared to Oct.31 (the last release day of Week 44). In terms of iron ore, market transactions were light at the beginning of the week, and market freight rates slightly fell. Subsequently, Australian miners actively inquired, pushing up market freight rates. The freight index for the Western Australia to Northern China route increased by 4.95% on a weekly basis. In contrast, the freight index for the Brazil to Tianjin route saw a smaller increase in the later part of the week, with a cumulative decrease of 0.31% this week. In terms of nickel ore, there were few nickel ore pallets, and the freight index for the Surigao to Tianjin route fell by 0.69% on a weekly basis.

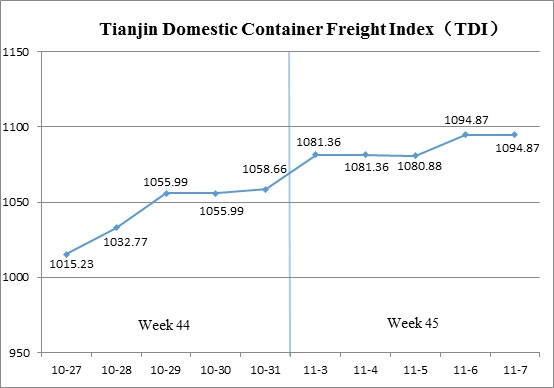

IV. Tianjin Domestic Container Freight Index (TDI)

In Week 45 (Nov.3 to Nov.7), the trend of the Tianjin Domestic Container Freight Index (TDI) is shown in the chart below:

In Week 45, the Tianjin Domestic Container Freight Index continued its upward trend.

On Nov.3 (Mon.), both the outbound and inbound indices recorded slight increases, driving the TDI to rise notably. The index then stabilized in the following days. From Nov.5 to 6 (Wed. to Thur.), the inbound index first declined and then rebounded, while the outbound index continued to climb. As a result, the TDI dipped slightly before recovering, and remained steady on Nov.7 (Fri.). Ultimately, the TDI closed at 1,094.87 points, marking a cumulative increase of 36.21 points, or 3.42%, compared with Oct.31 (the last release day of Week 44).

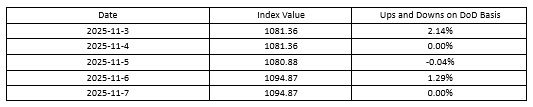

The TDI index value and several ups and downs on a day-on-day basis are as follows:

The Tianjin Domestic Container Outward Freight Index (TDOI) Continued to rise, closing at 1,162.56 points on Nov.7, an increase of 37.29 points or 3.31% compared with Oct.31 (the last release day of Week 44). Booking demand in Tianjin’s domestic coastal container market remained strong, and vessel capacity continued to be tight. Freight rates for routes bound for Fujian and South China sustained their upward momentum, with the Tianjin-Quanzhou/Xiamen and Tianjin-Guangzhou route indices closing at 1,380.50 points and 1,126.28 points, rising 5.25% and 3.21% week-on-week, respectively. In contrast, rates for the Tianjin-Shanghai route stabilized, with the index closing at 1,103.09 points, unchanged from the previous week.

The Tianjin Domestic Container Inward Freight Index (TDII) Continued to rise, surpassing the 1,000-point mark to close at 1,027.17 points on Nov.7, up 35.12 points or 3.54% compared with Oct.31 (the last release day of Week 44). In South China, vessel capacity remained tight, driving freight rates higher. The Guangzhou-Tianjin route index closed at 1,080.97 points, marking a 4.72% week-on-week increase. In contrast, freight rates in East China and Fujian stabilized, with the Shanghai-Tianjin and Quanzhou/Xiamen-Tianjin route indices closing at 1,061.42 points and 797.25 points, respectively, both unchanged from the previous week.

(The analysis report is for reference only and at your own risk)