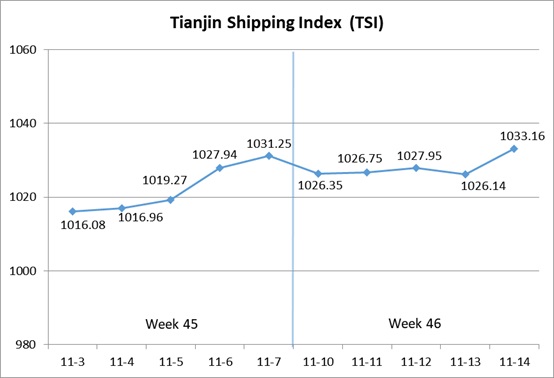

I. Tianjin Shipping Index (TSI)

In Week 46, 2025 (Nov.10 to Nov.14), Tianjin Container Freight Index (TCI) showed a weak performance. Tianjin Bulk Freight Index (TBI) decreased at first and then increased. Tianjin Domestic Container Freight Index (TDI) climbed steadily. The TSI fluctuated in a narrow range, eventually closing at 1033.16 points, with a cumulative increase of 1.91 points or 0.19% from Nov.7 (the last release day of Week 45). The trend of TSI is as follows:

The value and trend of TSI is as follows:

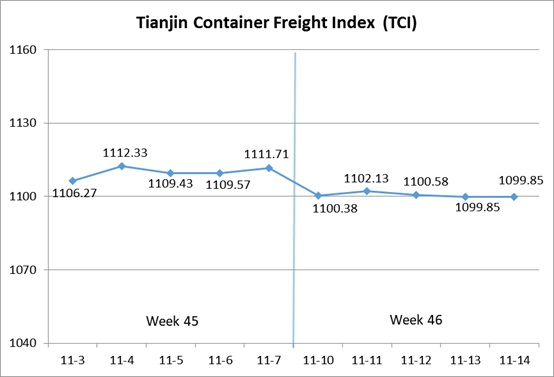

II. Tianjin Container Freight Index (TCI)

In Week 46, 2025 (Nov.10 to Nov.14), the trend of Tianjin Container Freight Index (TCI) is as follows:

In Week 46, the TCI saw a decline at the beginning of the week but remained stable overall.

From Nov.10-Nov.11 (Mon.-Tue.), the freight rates in European route and Mediterranean West route increased steadily, and the freight rates in Mediterranean East route and Central and South American route decreased slightly. The freight rates in American route, South American West route and South American East route decreased significantly. The freight rates in Thailand-Vietnam route and Indonesian route of Southeast Asia increased slightly. The TCI showed a weak performance, with a cumulative decrease of 0.86% on two releasing days. From Nov.12-Nov.14 (Wed.-Fri.), the freight rates in American route and South American West route decreased slowly, and the freight rates in Thailand-Vietnam route and Indonesian route of Southeast Asia continued to increase. The freight rates in European route, Mediterranean route, South American East route and Central and South American route kept steady. The TCI decreased slightly, with a cumulative decrease of 0.21% on three releasing days.

Finally, the TCI closed at 1099.85 points, with a cumulative decrease of 11.86 points (1.07%) from Nov.7 (the last release day of Week 45).

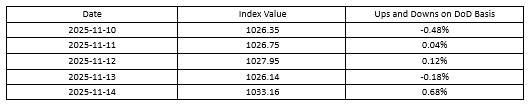

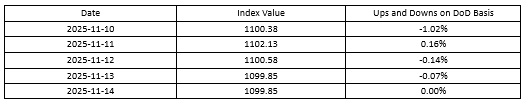

The TCI index value and several ups and downs on a day-on-day basis are as follows:

The TCI includes 19 sample routes. The main route analysis of this week is as follows:

European/Mediterranean route Freight rates saw mixed performance. For European route and Mediterranean West route, insufficient market cargo volume provided limited support for freight rates, resulting in a narrowed increase this week. The freight indices closed at 657.51 points and 1140.43 points, with the cumulative increase of 0.43% and 0.53%. For Mediterranean East route, weak demand for booking led some shipping companies to slightly reduce freight rates. The freight index closed at 863.73 points, with the decrease of 0.44% on a week-on-week basis.

American route As shipping capacity gradually recovered, shipping companies’ plan to raise prices in late November had not been implemented, and freight rates decreased. The freight indices in American West Coast route and American East Coast route closed at 900.48 points and 861.17 points, with the cumulative decrease of 7.54% and 5.35% in the week.

South American route Due to sluggish cargo volume and ample space supply, freight rates decreased significantly. The freight indices in South American West route and South American East route closed at 812.79 points and 1185.42 points, with the decrease of 19.63% and 12.13% on a week-on-week basis. In contrast, the Central and South American route market faced a shortage of light cargo, limiting the decline in the freight rate. The freight index closed at 1017.34 points, with the decrease of 1.79% on a week-on-week basis.

Southeast Asian route Affected by factors such as the peak transportation season and changes in local customs policies, ports such as Ho Chi Minh continue to be congested, and market freight rates continued to rise. The freight indices in Thailand-Vietnam route and Indonesian route closed at 474.25 points and 562.88 points, with the cumulative increase of 3.55% and 1.67% in the week.

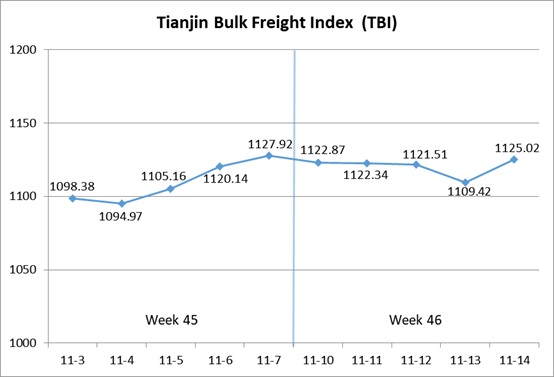

III. Tianjin Bulk Freight Index (TBI)

In Week 46, 2025 (Nov. 10 to Nov. 14), the trend of Tianjin Bulk Freight Index (TBI) was released as shown below:

In Week 46, the TBI first declined and then rose within the week.

From Nov. 10 to Nov. 13 (Mon. to Thur.), coal market freight rates fluctuated downward, grain market freight rates rose steadily, and metal ore market freight rates fell continuously, dragging the TBI down consecutively with a cumulative decrease of 1.64% over the four release days. On Nov. 14 (Fri.), grain market freight rates continued to rise, while coal and metal ore market freight rates rebounded slightly, driving the TBI to stop falling and stabilize, ultimately closed at 1125.02 points, with a cumulative decrease of 2.90 points or 0.26% compared to Nov. 7 (the last release day of Week 45).

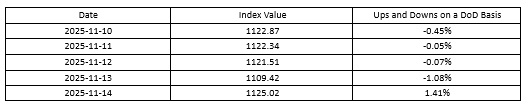

The TBI index value and several ups and downs on a day-on-day basis are as follows:

Tianjin Bulk Coal Freight Index (TBCI) Closed at 858.53 points, a cumulative increase of 6.30 points or 0.74% compared to Nov.7 (the last release day of Week 45). The growth in China’s coal import demand drove the market freight rates to rise slightly. In terms of the supramax market, Indonesian coal parcels consumed a large amount of shipping capacity, and the freight index for the Indonesia to Qingdao route rose continuously with a cumulative weekly increase of 1.17%. In the Capesize ship market, the freight index for the Hay Point to Qingdao route also showed an overall upward trend this week, with an increase of 0.49% on a weekly basis.

Tianjin Bulk Grain Freight Index (TBGI) Closed at 942.91 points, a cumulative increase of 1.76 points or 0.19% compared to Nov. 7 (the last release day of Week 45). The demand for coal and grain transportation remained stable, and the freight rates in the Panamax ship market were generally firm. The freight index for the South America to Tianjin route increased by 0.15% on a weekly basis, and the freight index for the US Gulf to Tianjin route rose by 0.17% on a weekly basis, and the freight index for the West America to Tianjin route went up by 0.37% on a weekly basis.

Tianjin Bulk Mineral Freight Index (TBMI) Closed at 1573.62 points, a cumulative decrease of 16.77 points or 1.05% compared to Nov.7 (the last release day of Week 45). In terms of iron ore, Australian miners adopted a wait-and-see attitude, and the transaction of Brazilian iron ore parcels was also sluggish. The overall market shipping capacity was sufficient, and the freight rates were under pressure to decline. The freight index for the Western Australia to Northern China route decreased by 1.33% on a weekly basis, and the freight index for the Brazil to Tianjin route fell by 1.07% cumulatively this week. In terms of nickel ore, the supramax ship capacity was consumed, and the freight index for the Surigao to Tianjin route stopped falling and rebounded by 0.87% on a weekly basis.

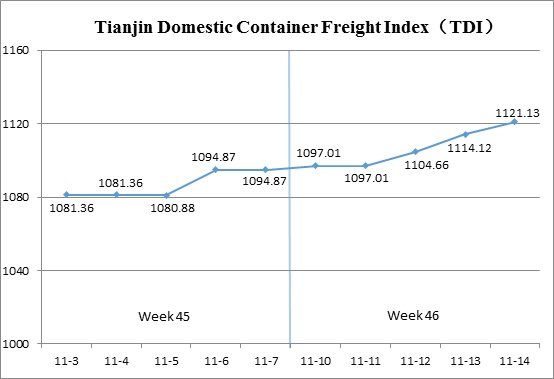

IV. Tianjin Domestic Container Freight Index (TDI)

In Week 46 (Nov.10 to Nov.14), the trend of the Tianjin Domestic Container Freight Index (TDI) is shown in the chart below:

In Week 46, the Tianjin Domestic Container Freight Index continued its upward trend.

From Nov.10 to 11 (Mon. to Tue.), the outbound index remained stable while the inbound index rose slightly, leading to a modest increase in the TDI. On Nov. 12 to 13 (Wed. to Thur.), the inbound index stabilized, and the outbound index continued to climb, pushing the TDI further upward. On Nov.14 (Fri.), both the inbound and outbound indices strengthened, driving the TDI higher once again and pushing it above the 1100-point mark. The TDI ultimately closed at 1121.13, representing a cumulative increase of 26.26 points, or 2.40%, compared with Nov.7 (the last release day of Week 45).

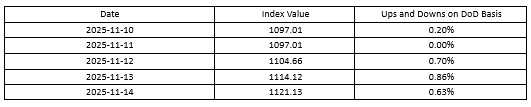

The TDI index value and several ups and downs on a day-on-day basis are as follows:

The Tianjin Domestic Container Outward Freight Index (TDOI) Continued to rise, closing at 1,200.21 points on Nov.14, an increase of 37.65 points or 3.24% compared with Nov.7 (the last release day of Week 45). In Tianjin’s outbound domestic container market, capacity on routes to Fujian remained tight, with booking demand staying robust. Freight rates were relatively stable in the early part of the week but advanced steadily toward the end. The Tianjin-Quanzhou/Xiamen route index closed at 1,437.88 points, up 4.16% week on week. On routes to South China, market sentiment was more cautious, and freight rates posted modest gains. The Tianjin-Guangzhou route index closed at 1,164.00 points, an increase of 3.50% week on week. Freight rates to East China remained stable, with the Tianjin-Shanghai route index closing at 1,103.09 points, unchanged week on week.

The Tianjin Domestic Container Inward Freight Index (TDII) Saw a slight increase, closing at 1,042.04 points on Nov. 14, up 14.87 points or 1.45% compared to Nov.7 (the last release day of Week 45). Operations at Nansha Terminal have resumed, though congestion remains, causing market freight rates to continue their upward trend. The Guangzhou-Tianjin route index closed at 1,095.67 points, marking a 1.36% increase week on week. Freight rates in the Fujian market remained stable with continued growth. The Quanzhou/Xiamen-Tianjin route index closed at 821.06 points, up 2.99% week on week. In the Shanghai market, rates remained steady, with the Shanghai-Tianjin route index closing at 1,061.42 points, unchanged week on week.

(The analysis report is for reference only and at your own risk)