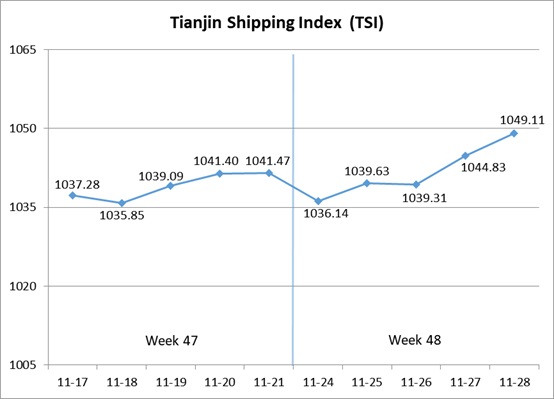

I. Tianjin Shipping Index (TSI)

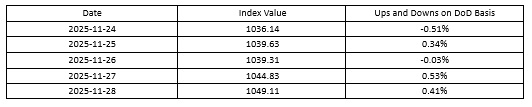

In Week 48, 2025 (Nov.24 to Nov.28), Tianjin Container Freight Index (TCI) decreased at first and then increased. Tianjin Bulk Freight Index (TBI) continued to increase. Tianjin Domestic Container Freight Index (TDI) fluctuated in a narrow range. The TSI fluctuated upwards, eventually closing at 1049.11 points, with a cumulative increase of 7.64 points or 0.73% from Nov.21 (the last release day of Week 47). The trend of TSI is as follows:

The value and trend of TSI is as follows:

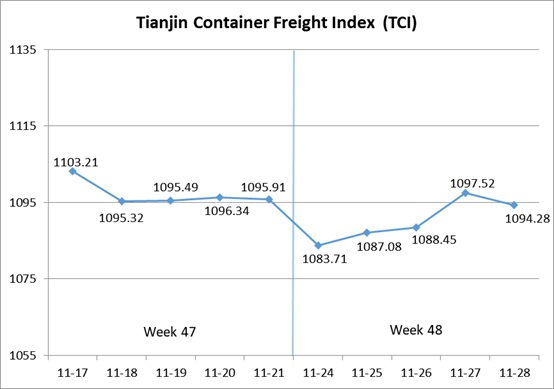

II. Tianjin Container Freight Index (TCI)

In Week 48, 2025 (Nov.24 to Nov.28), the trend of Tianjin Container Freight Index (TCI) is as follows:

In Week 48, the TCI decreased at first and then increased.

On Nov.24 (Mon.), the freight rates in Mediterranean route, American route, South American West route and South American East route showed weak performance, and the freight rates in European route, Thailand-Vietnam route and Indonesian route increased, and the freight rate in Central and South American route kept steady. The TCI dropped, with the decrease of 1.11%. From Nov.25-Nov.28 (Tue.-Fri.), the freight rate in European route increased at first and then decreased, and the freight rate in Mediterranean West route increased steadily, and the freight rate in Mediterranean East route kept steady. The freight rates in American route and South American East route decreased slightly, and the freight rates in South American West route, Central and South American route, Thailand-Vietnam route and Indonesian route showed strong performance. The TCI rebounded to last weekend’s level, with the cumulative increase of 0.98% on four releasing days.

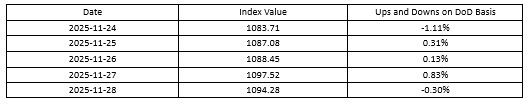

Finally, the TCI closed at 1094.28 points, with a cumulative decrease of 1.63 points (0.15%) from Nov.21 (the last release day of Week 47).

The TCI index value and several ups and downs on a day-on-day basis are as follows:

The TCI includes 19 sample routes. The main route analysis of this week is as follows:

European/Mediterranean route The freight rate performance was weak. On the European route, some shipping companies implemented a plan to increase freight rates in early December at the beginning of the week, resulting in a rapid increase in the freight rate. In the later part of the week, due to the weak willingness of other shipping companies or shipping alliances to follow up, the freight increase was not maintained, and the freight rate returned to a downward trend. The freight index closed at 671.03 points, with the decrease of 0.32% on a week-on-week basis. On the Mediterranean route, some shipping companies reduced their voyages, and the loading situation of liners was slightly better than that of the European route. The market freight rate showed a stable and slightly decreasing trend. The freight indices in Mediterranean East route and Mediterranean West route closed at 872.76 points and 1162.02 points, with the decrease of 1.00% and 0.29% on a week-on-week basis.

American route The spot cargo space remained high, and price reduction for cargo was still the mainstream in the market. In the middle and later stages of the week, there was an increase in market shipments, and the decline in freight rates narrowed. The freight indices in American West Coast route and American East Coast route closed at 731.31 points and 670.88 points, with the cumulative decrease of 2.90% and 7.81% in the week.

South American route Freight rates fluctuated. On the South American West route and Central and South American route, the congestion of ports in Mexico on the South American West route and the reduction of voyage schedules by some shipping companies led to a tightening of heavy container space on the Central and South American route. This week shipping companies’ plans to increase prices in early December had been implemented, driving freight rates to rise rapidly. The freight indices of the two routes closed at 775.92 points and 962.67 points respectively, with the cumulative increase of 12.35% and 4.27% during the week. On the South American East route, the early decline in the freight rate was relatively small, and the market cargo volume was insufficient. Some shipping companies launched special offer cabins to compete for cargo sources. The freight index closed at 1032.53 points, with the decrease of 4.36% on a week-on-week basis.

Southeast Asian route The market cargo volume remained high, but there was a shortage of containers on the Thailand-Vietnam route. At the same time, factors such as insufficient port operation equipment and severe weather led to port congestion, and ships were unable to unload in a timely manner upon arrival. As a result, freight rates continued to be strong this week. The freight indices in Thailand-Vietnam route and Indonesian route closed at 598.97 points and 638.31 points, with the cumulative increase of 16.82% and 7.52% in the week.

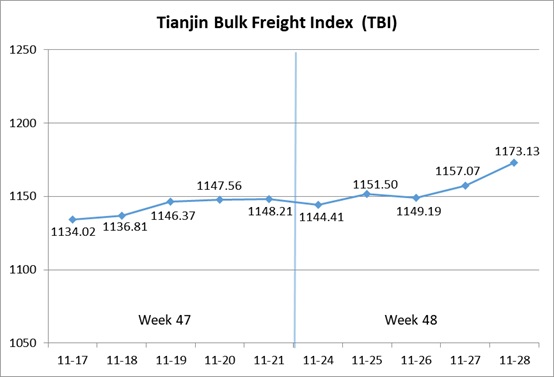

III. Tianjin Bulk Freight Index (TBI)

In Week 48, 2025 (Nov.24 to Nov.28), the trend of Tianjin Bulk Freight Index (TBI) was released as shown as follows:

In Week 48, the TBI further rose.

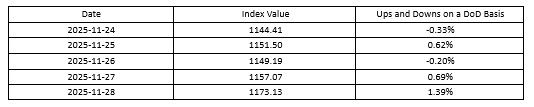

On Nov.24 (Mon.), grain market freight rates rose slightly, while coal and metal ore market freight rates fell back, leading to a 0.33% day-on-day decline in TBI. From Nov.25 to Nov.28 (Tue. to Fri.), coal market freight rates continued to rise slightly, while grain and metal ore market freight rates fluctuated upward. TBI fluctuated and advanced, ultimately closing at 1173.13 points, with a cumulative increase of 24.92 points or 2.21% compared to Nov.21 (the last release day of Week 47).

The TBI index value and several ups and downs on a day-on-day basis are as follows:

Tianjin Bulk Coal Freight Index (TBCI) Closed at 893.17 points, a cumulative increase of 20.21 points or 2.32% compared to Nov.21 (the last release day of Week 47). In terms of the Supramax market, transactions of Indonesian coal cargo parcels continued to perform well, significantly absorbing market shipping capacity. The freight index for the Indonesia to Qingdao route rose by 0.08% on a weekly basis.In terms of the Capesize market, the freight index for the Hay Point to Qingdao route increased by 3.58% on a weekly basis.

Tianjin Bulk Grain Freight Index (TBGI) Closed at 945.88 points, a cumulative increase of 0.25 points or 0.03% compared to Nov.21 (the last release day of Week 47). South American grain cargo parcels decreased, while US soybean transactions increased, resulting in mixed fluctuations in market freight rates. The freight index for the South America to Tianjin route fell by 0.86% on a weekly basis, the index for the US Gulf to Tianjin route rose by 0.50% on a weekly basis, and the index for the West America to Tianjin route increased by 0.73% on a weekly basis.

Tianjin Bulk Mineral Freight Index (TBMI) Closed at 1680.35 points, a cumulative increase of 54.31 points or 3.34% compared to Nov.21 (the last release day of Week 47). In terms of iron ore, Australian miners had active transactions, and spot shipping capacity in the Pacific region was tight, driving a significant rise in market freight rates. The freight index for the Western Australia to Northern China route increased by 4.89% on a weekly basis. Brazilian iron ore cargo transactions were moderate, and the freight index for the Brazil to Tianjin route first rose and then fell within the week, with a decrease of 0.39% on a weekly basis. In terms of nickel ore, rainy season factors continued to impact nickel ore shipments, but coal cargo parcels absorbed part of the Supramax ship capacity. The freight index for the Surigao to Tianjin route increased by 0.10% on a weekly basis.

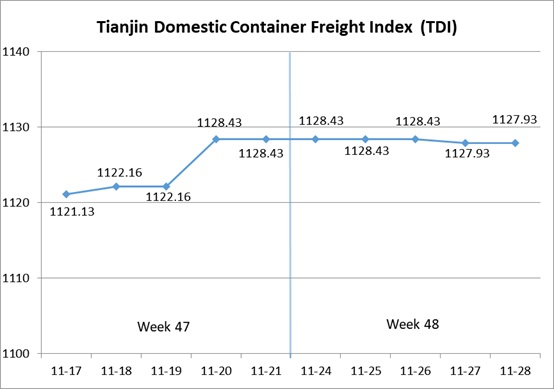

IV. Tianjin Domestic Container Freight Index (TDI)

In Week 48 (Nov.24 to Nov.28), the trend of the Tianjin Domestic Container Freight Index (TDI) is shown in the chart below:

In Week 48, the Tianjin Domestic Container Freight Index fell slightly.

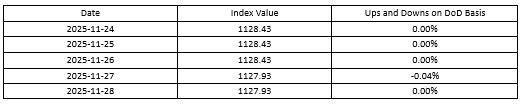

The inbound index remained stable this week, while the outbound index only weakly declined on Nov.27 (Thur.). The TDI fluctuated slightly and closed steadily at 1127.93 points on Nov.28 (Fri.), with a cumulative decrease of 0.50 points or 0.04% Compared to Nov.21 (the last release day of Week 47).

The TDI index value and day-on-day (DoD) change are as follows:

The Tianjin Domestic Container Outward Freight Index (TDOI) Slightly declined, closing at 1202.27 points on Nov.28, with a cumulative decrease of 1.00 point or 0.08% compared to Nov.21 (the last release day of Week 47). In the domestic trade containerization market for Tianjin's outbound shipments, the freight rate to Fujian slightly corrected. The freight index for the Tianjin to Quanzhou/Xiamen route closed at 1451.59 points, a week-on-week decrease of 0.46%. The freight rates from Tianjin to East China and South China continued to remain stable. The freight indices for the Tianjin to Shanghai route and Tianjin to Guangzhou route closed at 1103.09 points and 1164.00 points, respectively, and remained unchanged on a week on week basis.

The Tianjin Domestic Container Inward Freight Index (TDII) Returned to stability, closing at 1053.58 points on Nov.28, unchanged from Nov.21 (the last release day of Week 47). The overall freight rates in Tianjin's domestic trade container inbound market remained stable. The freight indices for the Shanghai to Tianjin route, Quanzhou/Xiamen to Tianjin route, and Guangzhou to Tianjin route closed at 1053.67 points, 821.06 points, and 1111.70 points, respectively, all remained unchanged on a week on week basis.

(The analysis report is for reference only and at your own risk)