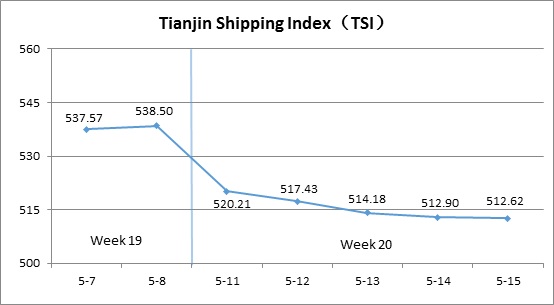

I. Tianjin Shipping Index (TSI)

Tianjin Shipping Index (TSI) was temporarily suspended from Feb.3 to May 6, and returned to normal from May 7 affected by COVID-19. In Week 19-20, 2020 (May 7 to May 15), TSI was released seven times. Tianjin Container Freight Index (TCI) fluctuated downwards. Tianjin Bulk Freight Index (TBI) rebounded slightly after the continuous decline. Tianjin Domestic Container Freight Index (TDI) continued to decrease. Tianjin Shipping Index (TSI) decreased continuously, and the TSI closed at 538.50 points with an increase of 0.17% on May 8 (the last release day of Week 19), and on May 15 (the last release day of Week 20), the TSI closed at 512.62 points with a decrease of 4.81% from May 8. The trend of TSI is as follows:

The chart above shows the trends of TSI from May 7, 2020 to May 15, 2020. The value of TSI in Week 19-20, 2020 is as follows:

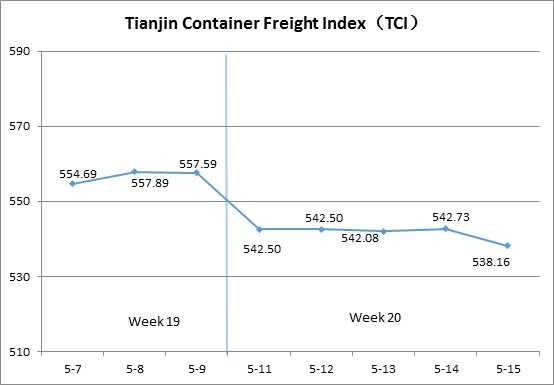

II. Tianjin Container Freight Index (TCI)

In Week 19-20, 2020 (May 7 to May 15), the trend of TCI is as follows:

In week 19-20, the TCI fluctuated downwards.

On May 7-9 (Thur.-Sat. in Week 19), the freight rates in European route, Mediterranean West route, East African route and West African route increased. The freight rate in American route kept steady. The freight rates in South American route and Persian Gulf route decreased. The TCI closed at 557.59 points from 554.69 points with an increase of 0.52%. On May 11-15 (Mon.-Fri. in Week 20), the freight rates in European route, Mediterranean route, American route and Persian Gulf route continued to decrease. The freight rates in South American route, East African route and West African route increased. The TCI continued to decrease, closing at 538.16 points with a decrease of 19.43 points (3.48%) from May 9 (the last release day of Week 19).

The TCI index value and several ups and downs on a day-on-day basis are as follows:

European/Mediterranean route In Week 19, shipowners in European route and Mediterranean East route market tried to raise freight rates slightly because of the gradual lifting of lockdowns in some countries such as Germany and Turkey. In Week 20, trader shipments remained low in the short term, and shipowners were under pressure to attract cargo, and rate decline to maintain cabin loading were still the mainstream of the market. The freight indices in European route, Mediterranean East route and Mediterranean West route closed at 385.83 points, 491.28 points and 501.88 points, with a decrease of 11.73%, 1.06% and 9.65% from May 9 (the last release day of Week 19).

American route Although many shipping companies reduced the supply of shipping capacity by means of returning ship chartering, reducing new ships, and suspending liners, the epidemic situation in the United States was still severe. More than half of the regions did not lift the lockdowns and restart. The market outlook was difficult to be optimistic. Shipping demand remained weak. Freight rates showed a steady and decreasing pattern within two weeks from Week 19 to Week 20. On May 15, the freight indices in the American East Coast route and the American West Coast route closed at 588.05 points and 640.62 points respectively, with a decrease of 0.57% and 1.92% from May 9 (the last release day of Week 19).

South American route In the early period, the epidemic situation in South America, especially in Brazil, was out of control. The shipping company planned to reduce the ship again from May to July, and the supply and demand relationship improved in this month. In addition, the international fuel price skyrocketed by more than 50% compared with the low level in the past half month, and the shipowners’ transportation cost increased. Freight rates rebounded after a slight decline at the beginning of Week 19. In Week 20, the index values in South American West route, South American East route and Central and South American route closed at 562.12 points, 769.77 points and 715.80 points, with an increase of 4.54%, 4.81% and 0.44% from May 9 (the last release day of Week 19).

Persian Gulf route In the Middle East, during the month of Ramadan, market transactions were sluggish, and there is a lack of light goods, and the freight gravity continued to move down within two weeks. The index value closed at 491.89 points, a cumulative decline of 5.93% from May 9 (the last release day of Week 19).

East African and West African route Africa’s epidemic prevention and control was better than expected, and the impact of the epidemic on the economy was relatively minor. Many Chinese companies began to resume normal operations locally. The demand for infrastructure materials, food, electrical appliances, mobile phones and other products gradually recovered. The freight rates remained strong in Week 19-20, increasing 3.83% and 3.70% in Week 19, and increasing 0.52% and 1.48% in Week 20.

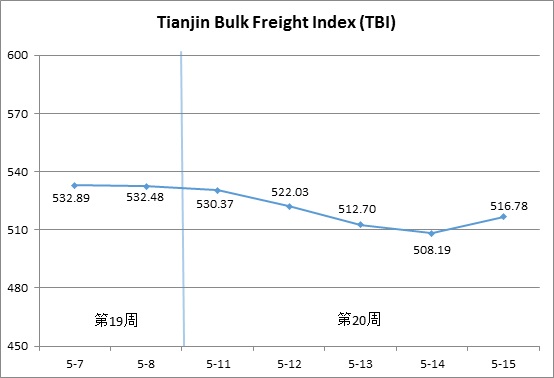

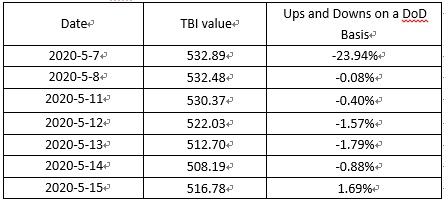

III. Tianjin Bulk Freight Index (TBI)

In the Week 19-Week 20 (May 7-May 15), the trend of the Tianjin Bulk Freight Index (TBI) for this week is shown in the chart below:

During the Week 19 -Week 20, the TBI totally showed a downward trend with a moderately stabilized rebound in this weekend.

Between May 7 and May 14 (Thursday Week 19 to Thursday Week 20), the freight rate of the grain declined slightly, and the freight rates of the coal and metal ore were in a weaken situation that caused the TBI continuing to drop for six release days, compared with a cumulative decrease of 4.64% on May 7. On May 15 (Friday), the freight rate of the grain continually decreased, and the rates of the coal and metal ore rebounded, prompting TBI increase by 1.69% on that day.

Finally, the TBI closed at 516.78 points, compared with a cumulative decrease of 15.70 points on May 8 (the last release day of the Week 19), and the cumulative decrease was 2.95%.

The value of the TBI and the DoD are shown below:

TBCI dropped continuously then rebounded rapidly at the weekend of the Week 20, and finally the value closed at 284.44 points. Compared with May 8 (the last release day of the Week 19), it decreased by the points of 7.07 (or 2.43%) cumulatively. In the Week 19, cement clinker, bauxite and other pallets freights were more than coal imports, and the freight rates continued to drop. With the accelerated progress of domestic resumption of production, the demand for imported coal increased in the late Week 20, and the coal import freight rate stopped falling and rebounded. In terms of Panamax, the demand for transportation in the whole market rose. In addition, some of the capacity had been placed in South America, and the freight rate of the route from Dalimpu Australia to Tianjin rebounded obviously, compared with an increase of nearly 0.2% on May 8. The freight rate of the Capesize market dropped sharply, and rebounded slightly in the late Week 20. The freight rate of the rout from High Point to Qingdao decreased by nearly 6% compared with May 8.

TBGI continuously dropped and finally closed at the points of 559.00 with a cumulative decrease of 12.54 points (or 2.19%) compared to May 8 (the last release day of the Week 19). After the Labor Day holiday, the increased demand for soybean export transportation in South America attracted a large amount of capacity, resulting in the accumulation of air transportation capacity and the lack of support for freight rates. The freight rate of the route from US Gulf to Tianjin has fallen by more than 3% compared to May 8, the freight rate of the route from South America to Tianjin has fallen by more than 1.2% compared to May 8, and the freight rate of the route from the West U.S. to Tianjin has been declined by nearly 1.3% compared to May 8.

TBMI declined first and then increased, but it was totally in a weak situation and the value finally closed at the points of 706.90. Compared to May 8 (the last release day of the Week 19), it dropped by the points of 27.48 (or 3.74%). In the Week 19, in terms of iron ore, there was a small amount of pallets in the Western Australia area, but there was an oversupply of the capacity in the Pacific market. The freight rate of the route from the Western Australia to Northern China decreased by nearly 5% compared with May 8. In terms of the situation in Brazil, the maintenance of berths at the Tubalao port significantly weakened the demand for long-distance mine transportation. The freight rate of the route from Brazil to Tianjin has fallen by nearly 8.5% compared to May 8. In the aspect of nickel ore, there were many pallets in the market, and the current shipping capacity was intense and the shipowner’s ability to increase price was enhanced. The freight rate of the route from Surigao to Tianjin increased by more than 4.5% during this week.

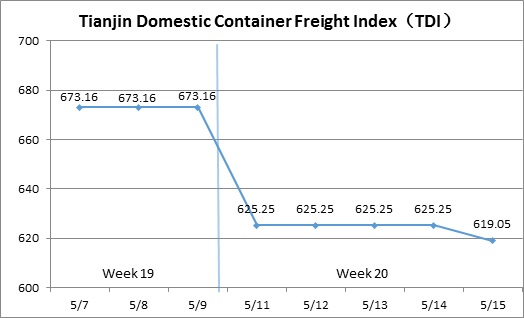

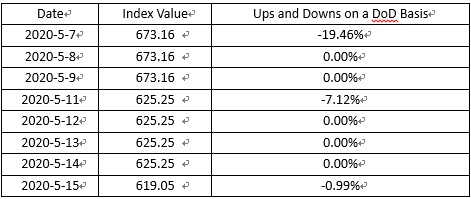

IV. Tianjin Domestic Container Freight Index (TDI)

In Week 19-20, 2020 (May 7-May 15), the trend of Tianjin Domestic Container Freight Index (TDI) is shown in the chart below.

In week 19-20, the TDI fell sharply.

From May 7- May 9 (Thursday to Saturday of week 19), the Outward Index and the Inward Index remained stable, so the TDI closed at 673.16 points. On May 11 (Monday, week 20), the outward index rebounded slightly, the inward index decreased sharply, dragging TDI down sharply, and the daily decrease was 7.12%. Subsequently, the inward index and the outward index returned to a stable level, and TDI stabilized at 625.25 points from May 12- May 14 (Tuesday to Thursday of week 20). On the May 15 (Friday of week 20), the outward index fell by 1.75%, and TDI continued to decline due to its impact and closed at 619.05 points, down 8.04% from May 9 (the last release day of week 19).

The TDI index value and several ups and downs on a day-on-day basis are as follows:

Tianjin Domestic Container Outward Freight Index (TDOI) rose first and then fell. The index value closed at 694.89 points on May 15, a decrease of 1.16% from May 9 (the last release day of week 19). The prevention and control of the COVID-19 has become normalized, localities are stepping up to resume production, and the trade market is gradually recovering. In week 19, the freight rate remained stable after the Labor Day holiday. At the beginning of the week 20, the outward route market picked up slightly. The Tianjin-Quanzhou / Xiamen route freight index rose slightly by 0.04% week-on-week, and the freight rate indices of Tianjin-Guangzhou route rose slightly by 0.79%. During the weekend, the freight rate of the Tianjin-Shanghai / Ningbo market was lower, with a significant correction. The index fell by 15.43% week-on-week.

Tianjin Domestic Container Inward Freight Index (TDII) fell sharply, and the index value closed on May 15 at 543.20 points, down 15.55% from May 9 (the last release day of week 19). In week 19, the market remained stable after the holidays. In the week 20, the freight rates of the Quanzhou / Xiamen-Tianjin route and the Shanghai / Ningbo-Tianjin route remained stable; the Guangzhou-Tianjin route had insufficient market capacity, and the market demand for home furnishing furniture for terminal consumption still needed to be improved. The competition for market supply was fierce, and freight rates dropped significantly, so the index value was 21.62% week-on-week.