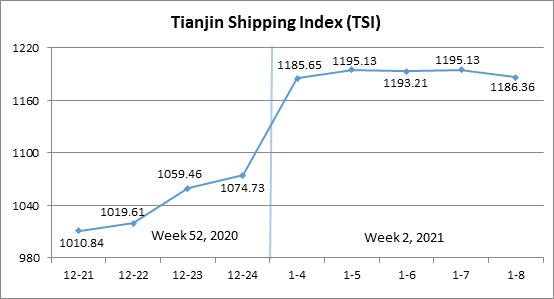

I. Tianjin Shipping Index (TSI)

In Week 2, 2021 (Jan.4 to Jan.8), Tianjin Container Freight Index (TCI)’s increase slowed down after the sharp increase. Tianjin Bulk Freight Index (TBI) continued to increase after the decrease at the beginning of the week. Tianjin Domestic Container Freight Index (TDI) decreased rapidly. Tianjin Shipping Index (TSI) fluctuated in a narrow range after the sharp increase. The TSI closed at 1186.36 points on Jan.8, with a cumulative increase of 10.39% from Dec.24, 2020 (the last release day of Week 52). The trend of TSI is as follows:

The chart above shows the trends of TSI from Dec.21, 2020 to Jan.8, 2021. The value of TSI in Week 2, 2021 is as follows:

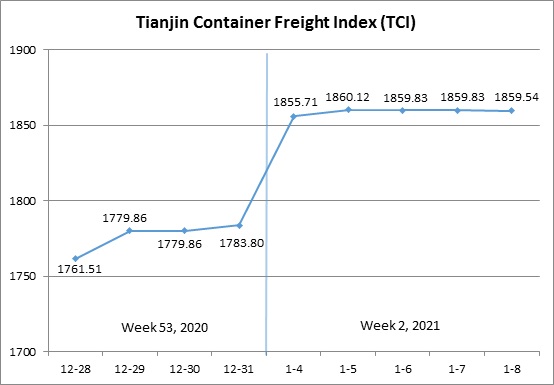

II. Tianjin Container Freight Index (TCI)

In Week 2, 2021 (Jan.4 to Jan.8), the trend of Tianjin Container Freight Index (TCI) is as follows:

In Week 2, the TCI kept steady after the sharp increase at the beginning of the week.

From Jan.4 to Jan.5 (Mon. to Tue.), the freight rates in European route, Mediterranean route, American route, South American route and West African route increased rapidly, and the freight rate in South African route increased slightly. The freight rate in East African route decreased slightly. The TCI increased 4.28% on two release days. From Jan.6 to Jan.8 (Wed. to Fri.), the freight rates in European route, Mediterranean route, American route, South American route and West African route kept steady. The freight rates in South African route and East African route decreased. The TCI decreased 0.03% on three release days. Finally, the TCI closed at 1859.54 points, with a cumulative increase of 75.74 points (4.25%) from Dec.31 (the last release day of Week 53).

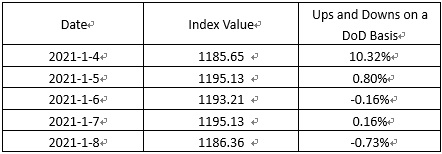

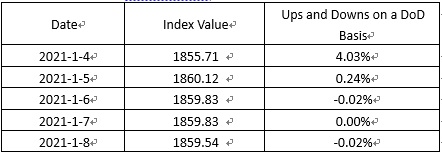

The TCI index value and several ups and downs on a day-on-day basis are as follows:

European/Mediterranean route In recent months, the production stagnation caused by the epidemic made the local area more dependent on imports of Chinese goods, and huge container transportation demand continued to push up freight rates to record increases. Entering the year of 2021, the market freight rate continued to increase, and the freight rate continued to rise sharply at the beginning of the week. Subsequently, the two major European freight associations called on the EU authorities to respond to the transportation market situation. At the same time, the China Shipowners’ Association convened a meeting with major liner companies this weekend to discuss stability measures of freight rates, and multiple factors temporarily stabilized the market freight rate in the second half of the week. Finally, the freight indices in European route, Mediterranean East route and Mediterranean West route closed at 1862.89 points, 1623.40 points and 2020.92 points, with the increase of 9.40%, 5.16% and 5.92% on a week-on-week basis. American route Affected by the epidemic, the inland transportation in the United States was extremely tight. Containers stored in the terminals could not be transported away in time. At the same time, a large number of ships were waiting at the port. Some liners needed to wait two weeks before entering the anchorage. The shipping company’s demurrage costs further increased, and the route rates continued to rise. The index values of American West Coast route and American East Coast route closed at 1566.46 points and 1344.31 points, with a cumulative increase of 2.63% and 4.32% respectively in the week.

South American route It was extremely difficult for empty containers stranded overseas to return. Many shipping companies sought to quickly expand the number of new containers, resulting in a serious shortage of new containers, which further promoted the cost of containers and drove the market freight rate to rise this week. The freight indices in South American West route, South American East route and Central and South American route closed at 2640.40 points, 3482.20 points and 2241.52 points, with the increase of 4.13%, 16.90% and 5.63% in the week.

African route Freight rates fluctuated. With the emergence of new COVID-19 viriant in South Africa, the market’s worries had been aggravated. Consumers continued to purchase and stock up, and transportation demand continued to increase, so freight rates continued to rise at the beginning of the week. In the second half of the week, some shippers’ shipments slowed down and freight rates decreased. The index value closed at 2933.69 points, up 0.69% on a week-on-week basis. The West African route market was affected by factors such as the epidemic and port extension project, so the port congestion was serious. Some shipping companies arranged for cargo to be transferred to nearby ports for unloading, which promoted a further increase in transportation costs. The index value closed at 3325.98 points, with an increase of 4.60% on a week-on-week basis. In contrast, the freight rate in East African route maintained a slight downward trend this week, and the index value closed at 2529.21 points, with a decrease of 0.32% on a week-on-week basis.

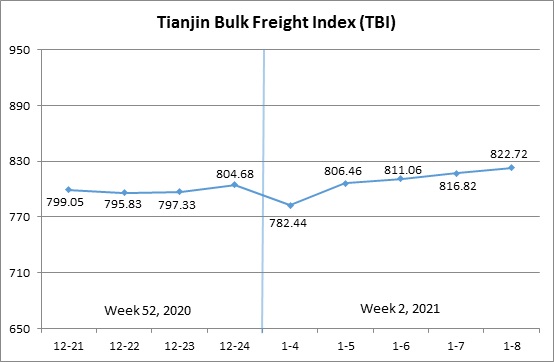

III. Tianjin Bulk Freight Index (TBI)

Week 2, 2021 (Jan.4-Jan.8), the trend of Tianjin Bulk Freight Index (TBI) is as follows:

In Week 2, the TBI decreased at first and then increased, and continued to rise in the latter period.

On Jan.4 (Mon.), the freight rates of coal, grain and metal ore decreased compared to that before the New Year’s Day holiday. The TBI decreased 2.76% on that day. On Jan.5 (Tue.), the freight rate of coal continued to decrease, and the freight rates of grain and metal ore increased, driving the TBI to increase 3.07% on a week-on-week basis. Afterwards, the freight rate of coal kept steady and increased, and the freight rates of grain and metal ore continued to increase, driving the TBI to increase slightly from Jan.6 to Jan.8.

Finally, the TBI closed at 822.72 points, with a cumulative increase of 18.04 points (2.24%) from Dec.24 (the last release day of Week 52).

TBI index value saw several ups and downs on a day-on-day basis, which is shown as follows:

TBCI dropped significantly after the New Year’s Day and stabilized later in the week, and it ended at 594.22 points, with a cumulative decrease of 30.21 points (4.84%) from Dec.24 (the last release day of Week 52). For Panamax vessels, during the New Year’s Day, the market was bleak, and freight rates continued to fall. With the continuous release of coal replenishment demand this week, Indonesian pallets increased significantly, and the market capacity was consumed greatly. The freight rate of Australia’s Darlingpu-Tianjin route rose slightly later in the week, with a decrease of 6% compared to that before the holiday. In the Capesize market, the freight rate of Hay Point to Qingdao route dropped significantly compared to that before the holiday. Although it fluctuated upwards during the week, it still had a cumulative drop of over 3%.

TBGI dropped slightly after New Year’s Day compared to that before the holiday, and continued to rise during the week. The index value finally closed at 708.15 points, with a cumulative increase of 28.72 points (4.23%) from Dec.24 (the last release day of Week 52). Grain futures prices increased, and traders increased their willingness to rent capacity, so market freight rates increased. The freight rate of South American-Tianjin route increased by nearly 6% this week. The freight rate of U.S. Gulf-Tianjin route increased by nearly 3.5% this week. The freight rate of West America-Tianjin route increased by nearly 2% this week.

TBMI fell significantly after New Year’s Day and continued to rise during the week. The index value finally closed at 1165.80 points, with a cumulative increase of 55.61 points (5.01%) from Dec.24 (the last release day of Week 52). For the iron ore market, during the New Year’s Day, transactions were bleak and market freight rates fell. After the holiday, severe weather in northern ports led to port pressure in some ports, reduced ship turnover and available capacity, and domestic iron ore purchase demand increased. Australian miners delivered shipments actively. The freight rate of West Australia-Northern China route climbed continuously during the week, with a cumulative increase of nearly 8.5%. In contrast, Brazil pallets were relatively sparse, and the freight rate of Brazil-Tianjin route fluctuated upwards during the week, but it was still lower than the level before the New Year’s Day holiday, with a cumulative drop of over 0.6%. As for the nickel ore, the freight rate of Surigao-Tianjin route dropped significantly at the beginning of the week compared to that before the holiday, and fluctuated within a narrow range during the week, with a cumulative drop of over 1.5% this week.

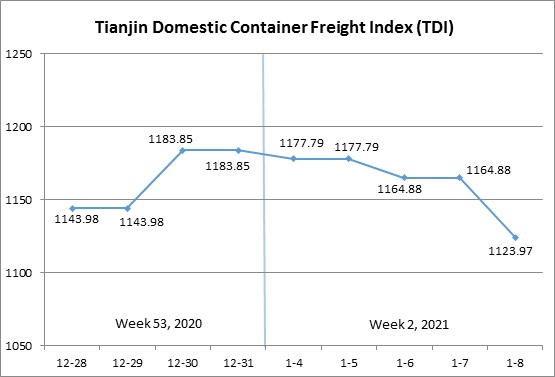

IV. Tianjin Domestic Container Freight Index (TDI)

In Week 2, 2021 (Jan.4 to Jan.8), the trend of Tianjin Domestic Container Freight Index (TDI) is shown in the chart below.

In Week 2, the Tianjin Domestic Container Freight Index (TDI) fell sharply.

On Jan.4 (Mon.), the outward index fell slightly, while the inward index remained stable, with a slight decline of 0.51% in TDI. Subsequently, the outward index and inward index fell rapidly one after another, showing a significant downward trend on Jan.6 (Wed.) and Jan.8 (Fri.) respectively, driving the TDI to continue to decline and finally close at 1123.97 points, with a decline of 59.88 points or 5.06% from Dec.31, 2020 (the last release day of Week 53, 2020).

The TDI index value and several ups and downs on a day-on-day basis are as follows:

The Tianjin Domestic Container Outward Freight Index (TDOI) fell slightly and closed at 1108.68 points on Jan.8, with a cumulative increase of 31.37 points or 2.75% from Dec.31, 2020 (the last release day of Week 53, 2020). After the New Year’s Day holiday, as the trading in the terminal market was quiet, the shipment of shippers slowed down, and the shipping demand was not strong. In the outward route market, the freight rates of Tianjin to Quanzhou/Xiamen, Tianjin to Shanghai/Ningbo and Tianjin to Guangzhou all dropped with varying degrees, and the index values fell by 6.60%, 4.10% and 1.59% on a week-on-week basis respectively.

The Tianjin Domestic Container Inward Freight Index (TDII) dropped significantly, and closed at 1139.26 points on Jan.8, down 88.39 points or 7.20% from Dec. 31, 2020 (the last release day of Week 53, of ). After the New Year’s Day holiday, the freight rate of Guangzhou to Tianjin route failed to maintain the rising level before the festival, showing a sharp decline, with the index value falling 8.53% on a week-on-week basis. The freight rate of Quanzhou/Xiamen to Tianjin route also decreased significantly, with the index value down 5.47% on a week-on-week basis. The freight rate of Shanghai/Ningbo route remained high level and stable, and the index value was flat on a week-on-week basis.