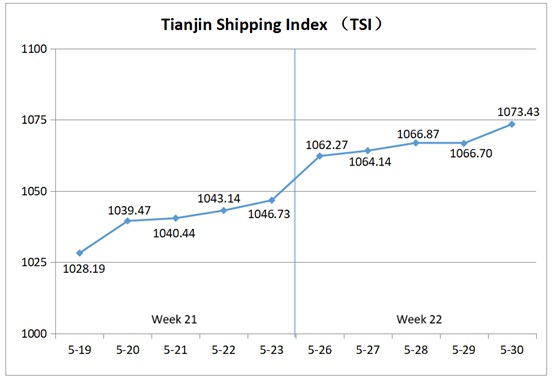

I. Tianjin Shipping Index (TSI)

In Week 22, 2025 (May 26 to May 30), Tianjin Container Freight Index (TCI) continued to rise, Tianjin Bulk Freight Index (TBI) fluctuated upward, Tianjin Domestic Container Freight Index (TDI) fell slightly. The Tianjin Shipping Index (TSI) climbed steadily and finally closed at 1,073.43 points, with a cumulative increase of 26.70 points (2.55%) compared to May 16(the last release day of Week 21). The trend of TSI is as follows:

The value and trend of TSI is as follows:

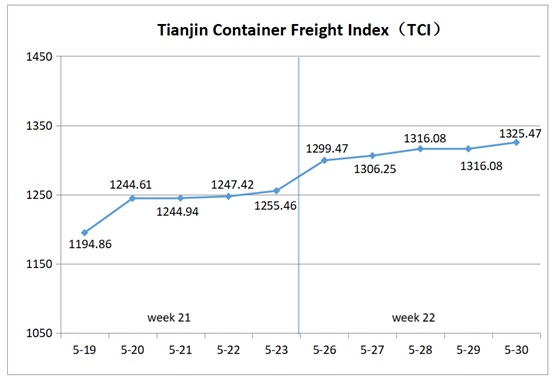

II. Tianjin Container Freight Index (TCI)

In Week 22, 2025 (May 26 to May 30), the trend of Tianjin Container Freight Index (TCI) is as follows:

In Week 22, the TCI continued its upward trend.

From May 26 (Mon.), the freight rates in European route increased slightly, while rates in Mediterranean, American, South American, and Persian Gulf routes surged sharply, driving the TCI up by 3.51% that day. Subsequently, the freight rates in European route stabilized briefly before declining, while rates in Mediterranean, American and Persian Gulf routes stabilized with slight increases, and rates on the South America route remained stable. The TCI continued to rise, with a cumulative increase of 2.00% from May 27 to 30 (Tue. to Fri.).

Finally, the TCI closed at 1,325.47 points, with a cumulative increase of 70.01 points or 5.58% compared with May 23(the last release day of Week 21).

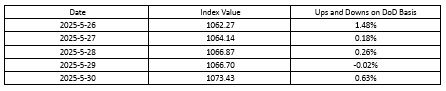

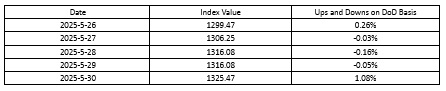

The TCI index value and several ups and downs on a day-on-day basis are as follows:

The TCI includes 19 sample routes. The main route analysis of this week is as follows:

European/Mediterranean route Freight rates showed divergent trends. Freight rate in the Europe route continued to rise at the beginning of the week, but then some shipping capacity returned to the route, causing the market freight rate to stabilize and then fall slightly, with the freight rate index finally closing at 674.40 points, down 0.97% week-on-week. For the Mediterranean route, after some shipping companies announced a new round of rate hikes, shippers accelerated their shipments before the new rates took effect, leading to tight cabin space. The freight indices for the Tianjin to East Mediterranean and Tianjin to West Mediterranean routes closed at 1153.72 points and 1501.09 points respectively, up 15.51% and 14.90% week-on-week.

American route Due to uncertainty over trade tariffs, importers accelerated order placements, and traders expedited shipments, driving strong booking demand. Shipping companies responded by reinstating previously canceled routes and launching new routes. This week, showed a strong upward trend. The freight indices for Tianjin to American West Coast and Tianjin to American East Coast routes closed at 1,403.59 points and 1,248.21 points respectively, up 20.00% and 16.21% week-on-week..

South American route Market cargo volume remained stable, but factors such as part of the capacity being deployed to the U.S. route, a truck driver strike at Callao Port causing cargo backlogs, and congestion at the Busan Port due to transshipment demand pushed rates significantly higher. The freight indices for Tianjin to West South America, East South America, and Central and South America closed at 1,038.48 points, 1,116.47 points, and 1,527.73 points respectively, up 19.22%, 12.01%, and 20.25% week-on-week.

Persian Gulf route Tight cabin space and shipping companies imposing restrictions on heavy cargo led to a strong rise in rates. The freight index closed at 903.49 points, up 8.75% week-on-week.

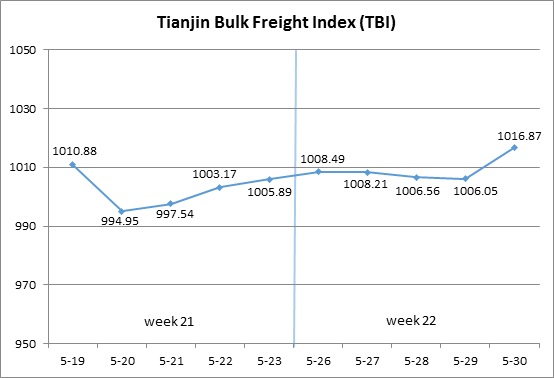

III. Tianjin Bulk Freight Index (TBI)

In Week 22, 2025 (May 26 to May 30), the trend of Tianjin Bulk Freight Index (TBI) was released as shown as follows:

In Week 22, the TBI fluctuated narrowly at the beginning of the week and rose significantly in the later part of the week.

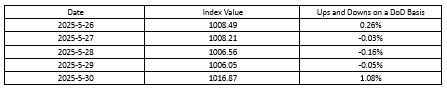

From May 26 to 29 (Mon. to Thur.), grain market freight rates continued to decline, while coal and metal ore market freight rates fluctuated narrowly. TBI first rose and then fell, with a cumulative increase of 0.02% over the four release days. Subsequently, the grain market freight rates further declined, while the coal and metal ore market freight rates rose, driving TBI to significantly increase on May 30 (Fri.) and ultimately close at 1016.87 points, a cumulative increase of 10.98 points or 1.09% compared to May 23 (the last release day of Week 21).

The TBI index value and several ups and downs on a day-on-day basis are as follows:

TBCI Closed at 759.56 points, a cumulative increase of 5.49 points or 0.73% compared to May 23 (the last release day of Week 21). In terms of the Supramax market, there is a shortage of coal cargo pallets, and the freight index for the Indonesia to Qingdao route has further declined, with a weekly decline of 1.84%. In terms of the Capsize market, the floods in eastern Australia have affected coal transportation, but the overall transportation demand in the market has improved, driving the freight index of the Hay Point to Qingdao route to fluctuate and rise, with a weekly increase of 2.37%.

TBGI Closed at 872.98 points, a cumulative decrease of 4.91 points or 0.56% compared to May 23 (the last release day of Week 21). The overall capacity of Panamax ships is abundant, and market freight rates continue to decline slightly. The freight index for the South American to Tianjin route decreased by 0.74% on a weekly basis, the freight index for the US Gulf to Tianjin route decreased by 0.44% on a weekly basis, and the freight index for the US West to Tianjin route decreased by 0.54% on a weekly basis.

TBMI Closed at 1418.07 points, a cumulative increase of 32.35 points or 2.33% compared to May 23 (the last release day of Week 21). In terms of iron ore, the transportation demand in Brazil has significantly increased, and Australian miners have actively inquired in the later part of the week, supporting market freight rates to rise. The freight index for the route from Western Australia to Northern China has fluctuated upwards, with a week on week increase of 2.80%. The freight index for the route from Brazil to Tianjin continues to rise, with a week on week increase of 3.91%. In terms of nickel ore, there were few transactions of nickel ore pallets in the Philippines, and the freight index of the Surigao to Tianjin route fell by 3.28% week on week.

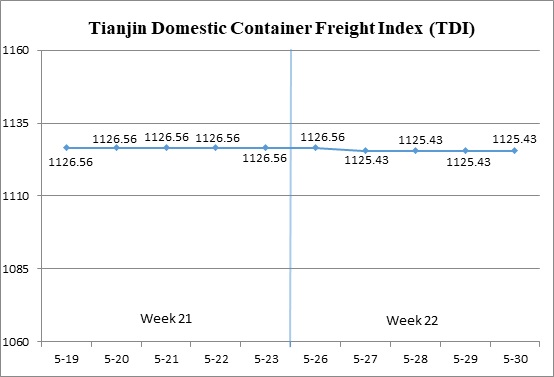

IV. Tianjin Domestic Container Freight Index (TDI)

In Week 22 (May 26 to May 30), the trend of the Tianjin Domestic Container Freight Index (TDI) is shown below:

In Week 22, the Tianjin Domestic Container Freight Index experienced a slight decline.

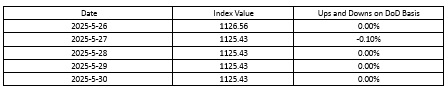

The outbound index remained stable throughout the week, while the inbound index recorded a minor drop on May 27 (Tue.). As a result, the TDI edged down slightly, closing at 1125.43 points, marking a cumulative drop of 1.13 points or 0.10% compared to May 23 (the last release day of Week 21) .

The TDI index value and several ups and downs on a day-on-day basis are as follows:

The Tianjin Domestic Container Outward Freight Index (TDOI) Remained stable, closing at 1076.42 points on May 30, unchanged from May 23 (the last release day of Week 21). Amid accelerated coal yard clearance and outbound shipments, freight rates in Tianjin’s domestic container shipping market held steady. The freight indices for the Tianjin to Guangzhou, Tianjin to Quanzhou/Xiamen, and Tianjin to Shanghai routes closed at 1053.44 points, 1162.66 points, and 1135.83 points respectively, all flat on a week-over-week basis.

The Tianjin Domestic Container Inward Freight Index (TDII) Continued its slight downward trend, closing at 1174.44 points on May 30, which is a cumulative decline of 2.25 points or 0.19%, compared to May 23 (the last release day of Week 21). Freight rates in the Fujian market saw a modest decline this week, with the Quanzhou/Xiamen to Tianjin route index falling to 932.35 points, down 1.32% week-over-week. In contrast, rates in East and South China remained stable. The freight indices for the Shanghai to Tianjin and Guangzhou to Tianjin routes closed at 1061.42 and 1250.66 points, respectively, both unchanged from the previous week.

(The analysis report is for reference only and at your own risk)