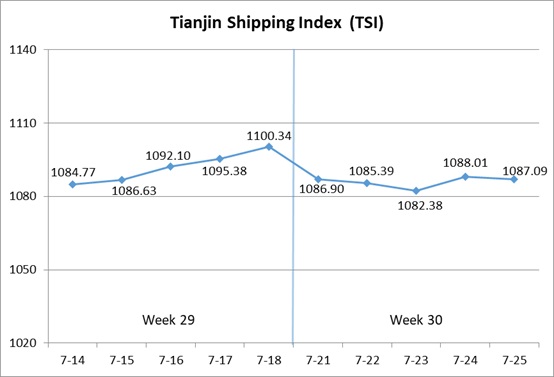

I. Tianjin Shipping Index (TSI)

In Week 30, 2025 (Jul.21 to Jul.25), Tianjin Container Freight Index (TCI) continued to decrease. Tianjin Bulk Freight Index (TBI) increased steadily. Tianjin Domestic Container Freight Index (TDI) decreased slightly. The TSI decreased rapidly at the beginning of the week and then fluctuated in a narrow range, eventually closing at 1087.09 points, with a cumulative decrease of 13.25 points or 1.20% from Jul.18 (the last release day of Week 29). The trend of TSI is as follows:

The value and trend of TSI is as follows:

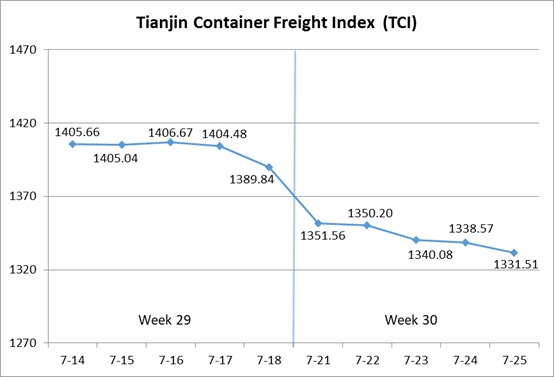

II. Tianjin Container Freight Index (TCI)

In Week 30, 2025 (Jul.21 to Jul.25), the trend of Tianjin Container Freight Index (TCI) is as follows:

In Week 30, the TCI continued to decrease.

From Jul.21-Jul.23 (Mon.-Wed.), the freight rate in European route increased at first and then decreased, and the freight rates in Mediterranean route, South American West route, South American East route, Indonesian route, Thai-Vietnamese route decreased slightly. The freight rates in American route and Central and South American route decreased greatly. The TCI decreased significantly, with a cumulative decrease of 3.58% on three releasing days. From Jul.24-Jul.25 (Thur.-Fri.), the freight rate in European route stopped falling and rebounded, and the freight rates in Mediterranean route, American route, South American East route, Indonesian route, Thai-Vietnamese route decreased steadily. The freight rates in South American West route and Central and South American route kept steady. The TCI continued to decrease, with a cumulative decrease of 0.64% on two releasing days.

Finally, the TCI closed at 1331.51 points, with a cumulative decrease of 58.33 points (4.20%) from Jul.18 (the last release day of Week 29).

The TCI index value and several ups and downs on a day-on-day basis are as follows:

The TCI includes 19 sample routes. The main route analysis of this week is as follows:

European/Mediterranean route Some shipping companies on the European route slightly increased freight rates, but the market’s willingness to follow suit was not strong. The freight rate closed at 1049.82 points, with the decrease of 0.45% on a week-on-week basis. The Mediterranean route market introduced low-price cabins, and freight rates continued to fall. The freight indices in Mediterranean East route and Mediterranean West route closed at 1049.34 points and 1350.83 points, with the decrease of 3.64% and 2.30% on a week-on-week basis.

American route The shipping demand remained sluggish, and market freight rates continued to decrease. The freight indices in American West Coast route and American East Coast route closed at 840.44 points and 944.29 points, with the decrease of 5.73% and 13.88% on a week-on-week basis.

South American route On the South American East route, the freight rate recently rose to the highest point since this year, leading to a decrease in shippers’ willingness to book space. This week the freight rate began to decrease. The freight rate closed at 2849.29 points, with the decrease of 1.62% on a week-on-week basis. On the South American West route and Central and South American route, market volume continued to fall. The freight indices of two routes closed at 940.82 points and 1407.54 points, with the decrease of 1.77% and 3.18% on a week-on-week basis.

Southeast Asian route Shipping companies launched preferential measures to actively compete for cargo sources, and market freight rates continued to decrease. The freight indices in Indonesian route and Thai-Vietnamese route closed at 678.30 points and 519.02 points, with the decrease of 2.43% and 2.30% on a week-on-week basis.

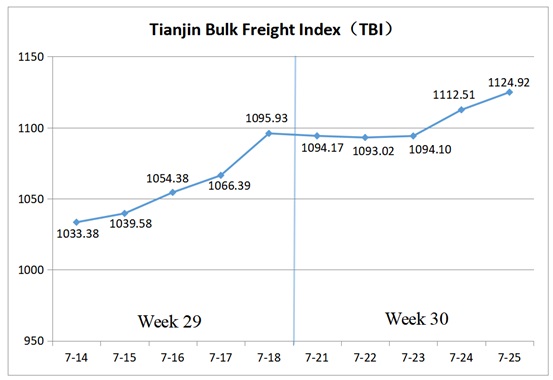

III. Tianjin Bulk Freight Index (TBI)

In Week 30, 2025 (July 21 to July 25), the trend of Tianjin Bulk Freight Index (TBI) was released as shown as follows:

In Week 30, the TBI showed a steady trend at the beginning of the week, followed by consecutive increases in the latter part.

From July 21 to July 23 (Mon. to Wed.), freight rates in the coal, grain, and metal ore markets experienced minor fluctuations with a slight downward trend, leading to a marginal decline in the TBI, which dropped by 0.17% over the three release days. Subsequently, freight rates in the grain market declined further, while those in the coal and metal ore markets rose rapidly, driving the TBI to increase further. The index ultimately closed at 1124.92 points, marking a cumulative increase of 28.99 points (or 2.65%) compared to July 18 (the last release day of Week 29).

The TBI index value and several ups and downs on a day-on-day basis are as follows:

Tianjin Bulk Coal Freight Index (TBCI) Closed at 835.79 points, a cumulative increase of 19.46 points (2.38%) compared to July 18 (the last release day of Week 29). In terms of Supramax market, coal shipping demand in Southeast Asia declined slightly, narrowing the increase in the freight index for the Indonesia to Qingdao route, which rose by 0.27% week-on-week. The Capesize ship market saw an overall increase in freight rates, with the freight index for the Hay Point to Qingdao route rising by 3.69% week-on-week.

Tianjin Bulk Grain Freight Index (TBGI) Closed at 942.15 points, a cumulative decrease of 2.35 points (0.25%) compared to July 18 (the last release day of Week 29). Demand for soybean shipments from South American gradually weakened, leading to a cooling Panamax market and a decline in freight rates. The freight index for the South America to Tianjin route fell by 0.75% week-on-week, and the index for the US West Coast to Tianjin route dropped by 0.13% week-on-week. In contrast, the freight index for the US Gulf to Tianjin route rose by 0.09% week-on-week.

Tianjin Bulk Mineral Freight Index (TBMI) Closed at 1596.83 points, a cumulative increase of 69.88 points (4.58%) compared to July 18 (the last release day of Week 29). In terms of iron ore, the market was generally quiet at the beginning of the week. However, in the latter part of the week, inquiries from Australian miners increased, cargo transactions in the Brazilian market improved, and FFA (Forward Freight Agreement) prices rose, driving up spot market freight rates. The freight index for the West Australia to Northern China route rose by 5.12% week-on-week, and the index for the Brazil to Tianjin route increased by 5.22% week-on-week. For nickel ore, typhoon weather affected nickel ore shipments, causing the freight index for the Surigao to Tianjin route to fall by 0.12% week-on-week.

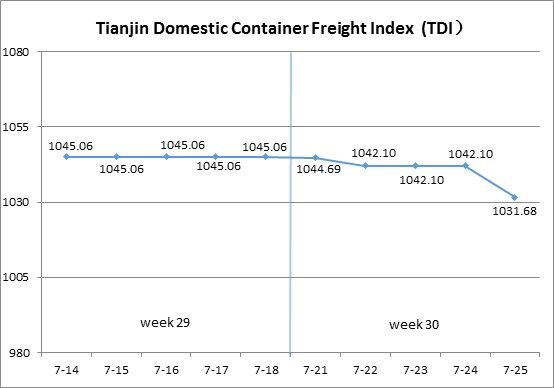

IV. Tianjin Domestic Container Freight Index (TDI)

In Week 30 (July 21 to July 25), the trend of the Tianjin Domestic Container Freight Index (TDI) is shown in the chart below:

In Week 30, the Tianjin Domestic Container Freight Index declined slightly.

From July 21 to July 22 (Mon. to Tue.), the outbound index rose and then fell, while the inbound index slightly declined, and TDI continued to decline. From July 23 to July 24 (Wed. to Thur.), the outbound and inbound indices returned to stable levels. On July 25 (Fri.), the outbound index rose slightly, while the inbound index fell significantly, dragging the decline of TDI to expand and ultimately closing at 1031.68 points, with a cumulative decline of 13.38 points or 1.28% compared to July 18 (the last release day of Week 29).

The TDI index value and several ups and downs on a day-on-day basis are as follows:

The Tianjin Domestic Container Outward Freight Index (TDOI) Rose weakly, closing at 950.71 points on July 25, a cumulative increase of 4.86 points or 0.51% compared to July 18 (the last release day of Week 29). This week, the transportation capacity was relatively tight, with a slight increase in transport volume and good loading conditions on ships. The freight rates in the Tianjin outbound containerized transport market fluctuated slightly. The freight index for the Tianjin to Guangzhou route slightly increased, closing at 918.81 points, with a week on week increase of 0.99%; The freight rates for the Tianjin to Quanzhou/Xiamen route showed a slight increase at the beginning of the week, followed by a significant decline, and then rebounded slightly in the later part of the week. The freight index closed at 1029.36 points, a decrease of 1.35% compared to the previous week; The freight rates for the Tianjin to Shanghai route remained stable, with the freight index closing at 1110.30 points, unchanged from the previous week.

The Tianjin Domestic Container Inward Freight Index (TDII) Significantly declined, closing at 1112.64 points on July 25, a cumulative decrease of 31.62 points or 2.76% compared to July 18 (the last release day of Week 29). Affected by typhoon factors, the frequency of ship schedules was unstable, shippers’ shipments were delayed, and market freight rates decreased. The freight rates for the Guangzhou to Tianjin route significantly declined, with the freight index closing at 1167.80 points, a decrease of 3.51% on a weekly basis; The freight rates for the Quanzhou/Xiamen to Tianjin route slightly decreased, with the freight index closing at 920.44 points, a week on week decrease of 0.64%; The freight rate index for the Shanghai to Tianjin route closed at 1061.42 points, unchanged from the previous week.

(The analysis report is for reference only and at your own risk)