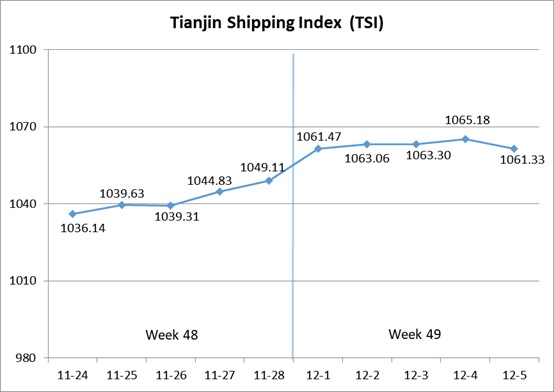

I. Tianjin Shipping Index (TSI)

In Week 49, 2025 (Dec.1 to Dec.5), Tianjin Container Freight Index (TCI) experienced a rapid rise followed by a narrow range consolidation. Tianjin Bulk Freight Index (TBI) continued to increase. Tianjin Domestic Container Freight Index (TDI) continued to decrease. The TSI fluctuated at high levels, eventually closing at 1061.33 points, with a cumulative increase of 12.22 points or 1.16% from Nov.28 (the last release day of Week 48). The trend of TSI is as follows:

The value and trend of TSI is as follows:

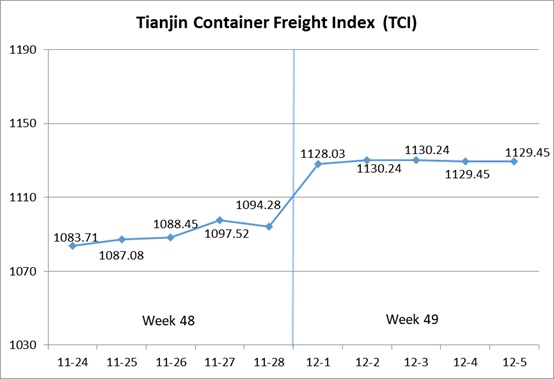

II. Tianjin Container Freight Index (TCI)

In Week 49, 2025 (Dec.1 to Dec.5), the trend of Tianjin Container Freight Index (TCI) is as follows:

In Week 49, the TCI increased at the beginning of the week and then kept steady.

From Dec.1-Dec.2 (Mon.-Tue.), the freight rates in Mediterranean route, American East Coast route, South American route, Thailand-Vietnam route and Indonesian route increased significantly, and the freight rate in European route increased slightly, and the freight rate in American West Coast route decreased slightly. The TCI increased rapidly, with the cumulative increase of 3.29% on two releasing days. From Dec.3-Dec.5 (Wed.-Fri.), the freight rates in European route, Mediterranean route and Indonesian route kept steady, and the freight rates in American West Coast route and Thailand-Vietnam route increased slightly, and the freight rates in American East Coast route and South American route showed weak performance. The TCI fluctuated in a narrow range, with the cumulative decrease of 0.07% on three releasing days.

Finally, the TCI closed at 1129.45 points, with the cumulative increase of 35.17 points (3.21%) from Nov.28 (the last release day of Week 48).

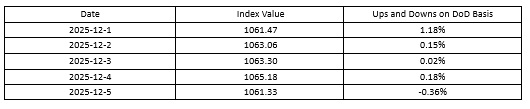

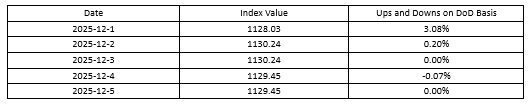

The TCI index value and several ups and downs on a day-on-day basis are as follows:

The TCI includes 19 sample routes. The main route analysis of this week is as follows:

European/Mediterranean route On the Mediterranean route, the shipping company’s freight increase plan for this month had been implemented, and the overall performance of freight rates was strong. The freight indices in Mediterranean East route and Mediterranean West route closed at 930.91 points and 1191.37 points, with the increase of 6.66% and 2.53% on a week-on-week basis. On the European route, the main basic ports remained congested, and market cargo volume continued to hover at a low level. The freight rate showed a slight upward trend this week. The freight index closed at 671.09 points, with the increase of 0.01% on a week-on-week basis.

American route The freight rates showed divergent trends. On the American West Coast route, weak factory demand led to the failure of shipping companies’ planned rate hikes. As the previous rates had been falling continuously, the carriers were unwilling to significantly reduce prices further, resulting in a slightly declining and volatile freight rate. The freight index closed at 728.39 points, with the decrease of 0.40% on a week-on-week basis. On the American East Coast route, with carriers reducing sailings, the freight rate strengthened notably at the beginning of the week. However, insufficient market volume caused the freight rate to decline subsequently. The freight index closed at 711.72 points, with the increase of 6.09% on a week-on-week basis.

South American route The factory shipment volume rebounded, and market space was tight. The port strike in Mexico caused terminal congestion, prompting shipping companies to continue raising freight rates at the beginning of the week. Subsequently, some carriers reduced prices to improve space utilization, leading to a slight decline in freight rates. The freight indices in South American West route and Central and South American route closed at 818.31 points and 1001.77 points, with the increase of 5.46% and 4.06% on a week-on-week basis. On the South American East route, the freight rate increased at first and then decreased. The freight index closed at 1032.53 points, remaining flat on a week-on-week basis.

Southeast Asian route The high booking demand, coupled with factors such as the peak season’s concentrated cargo arrivals and a shortage of port handling equipment, led to continued congestion at Ho Chi Minh Port. Freight rates extended their upward trend this week. The freight indices in Thailand-Vietnam route and Indonesian route closed at 639.63 points and 729.05 points, with the cumulative increase of 6.79% and 14.22% in the week.

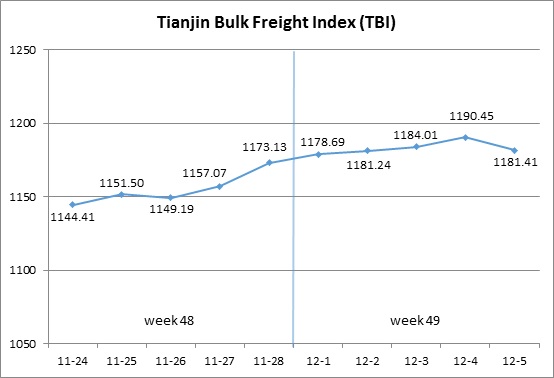

III. Tianjin Bulk Freight Index (TBI)

In Week 49, 2025 (Dec.1 to Dec.5), the trend of Tianjin Bulk Freight Index (TBI) was released as shown as follows:

In Week 49, TBI further rose and slightly fell in the later part of the week.

From Dec.1 to Dec.4 (Mon. to Thur.), grain market freight rates slightly decreased, and coal market freight rates continued to rise slightly, and metal ore market freight rates continued to rise, and TBI continued to rise for four consecutive release days, with a cumulative increase of 1.48%. On Dec.5 (Fri.), grain market freight rates continued to be weak, while coal and metal ore market freight rates turned from rising to falling. TBI slightly fell and finally closed at 1181.41 points, a cumulative increase of 8.28 points or 0.73% compared to Nov.28 (the last release day of Week 48).

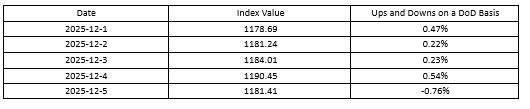

The TBI index value and several ups and downs on a day-on-day basis are as follows:

Tianjin Bulk Coal Freight Index (TBCI) Closed at 898.60 points, a cumulative increase of 5.43 points or 0.61% compared to Nov.28 (the last release day of Week 48). In terms of the supramax market, there was a significant increase in coal cargo in Southeast Asia, and the immediate transportation capacity was relatively tight. The freight index from Indonesia to Qingdao rose by 0.88% on a weekly basis. In terms of the Capsize market, the freight index of the Hay Point to Qingdao route also continued to rise, with a weekly increase of 0.46%.

Tianjin Bulk Grain Freight Index (TBGI) Closed at 939.1 points, a cumulative decrease of 6.47 points or 0.68% compared to Nov.28 (the last release day of Week 48). The number of grain pallets in South America further decreased, leading to an increase in market wait-and-see sentiment and a continuous decline in market freight rates. The freight index for the South American to Tianjin route decreased by 1.01% on a weekly basis, the freight index for the US Gulf to Tianjin route decreased by 0.54% on a weekly basis, and the freight index for the West America to Tianjin route decreased by 0.30% on a weekly basis.

Tianjin Bulk Mineral Freight Index (TBMI) Closed at 1706.22 points, a cumulative increase of 25.87 points or 1.54% compared to Nov.28 (the last release day of Week 48). In terms of iron ore, the increase in inquiries from Australian miners and active market transactions drove up FFA forward contract prices and long-distance mining route freight rates. The freight index for the Western Australia to Northern China route increased by 1.61% on a weekly basis, and the freight index for the Brazil to Tianjin route increased by 1.89% on a weekly basis. In terms of nickel ore, the freight index of the Surigao to Tianjin route slightly increased, with a cumulative increase of 0.34% this week.

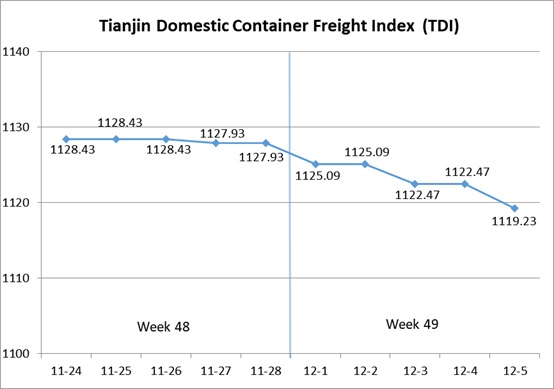

IV. Tianjin Domestic Container Freight Index (TDI)

In Week 49 (Dec.1 to Dec.5), the trend of the Tianjin Domestic Container Freight Index (TDI) is shown in the chart below:

In Week 49, the Tianjin Domestic Container Freight Index continued to record modest declines.

On Dec.1 (Mon.), the inbound index edged down while the outbound index posted a slight increase, resulting in a marginal dip in the TDI before it stabilized. On Dec.3 and 5 (Wed. and Fri.), the inbound index extended its downward trend and the outbound index retreated, leading the TDI to decline further. The index ultimately closed at 1119.23 points, representing a cumulative decrease of 8.70 points, or 0.77%, compared with Nov. 28 (the last release day of Week 48).

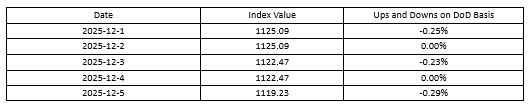

The TDI index value and several ups and downs on a day-on-day basis are as follows:

The Tianjin Domestic Container Outward Freight Index (TDOI) Rose slightly before edging down again, closing at 1197.73 points on Dec.5, a cumulative decrease of 4.54 points, or 0.38%, compared with Nov.28 (the last release day of Week 48). In North China, equipment maintenance at several steel enterprises and weak trading prices softened booking demand on Tianjin’s domestic coastal services to South China and Southwest China, leading to a modest decline in freight rates. The Tianjin-Guangzhou route index closed at 1155.59 points, down 0.72% week on week. Supported by cargo volumes, freight rates to Fujian recorded a mild rebound, with the Tianjin-Quanzhou/Xiamen route index closing at 1464.53 points, up 0.89% week on week. Rates on Tianjin-Shanghai services remained stable, with the index closing at 1103.09 points, unchanged from the previous week.

The Tianjin Domestic Container Inward Freight Index (TDII) Edged lower, closing at 1040.73 points on Dec.5, a cumulative decline of 12.85 points, or 1.22%, compared with Nov.28 (the last release day of Week 48). Inbound rates from East China and Fujian to Tianjin fell noticeably, with the Shanghai–Tianjin and Quanzhou/Xiamen-Tianjin route indices closing at 1001.36 points and 778.73 points, down 4.96% and 5.16% week on week, respectively. In contrast, rates from South China to Tianjin remained stable, with the Guangzhou-Tianjin route index closing at 1111.70 points, unchanged from the previous week.

(The analysis report is for reference only and at your own risk)