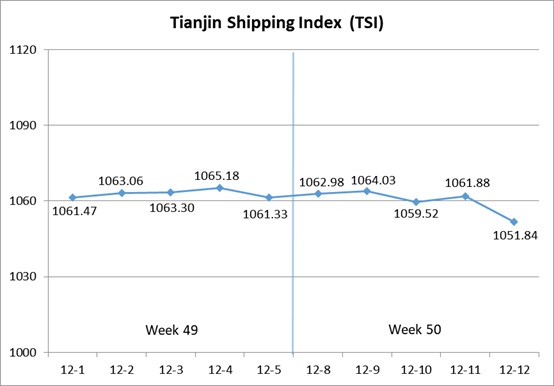

I. Tianjin Shipping Index (TSI)

In Week 50, 2025 (Dec.8 to Dec.12), Tianjin Container Freight Index (TCI) fluctuated upwards. Tianjin Bulk Freight Index (TBI) decreased rapidly. Tianjin Domestic Container Freight Index (TDI) fluctuated in a narrow range. The TSI decreased slightly, eventually closing at 1051.84 points, with a cumulative decrease of 9.49 points or 0.89% from Dec.5 (the last release day of Week 49). The trend of TSI is as follows:

The value and trend of TSI is as follows:

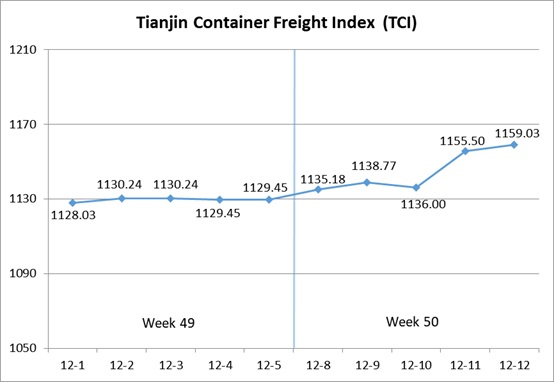

II. Tianjin Container Freight Index (TCI)

In Week 50, 2025 (Dec.8 to Dec.12), the trend of Tianjin Container Freight Index (TCI) is as follows:

In Week 50, the TCI increased slightly and then increased rapidly.

From Dec.8-Dec.10 (Mon.-Wed.), the freight rates in European route and Mediterranean route increased steadily, and the freight rates in American route and South American route were under pressure and decreased. The freight rate in Indian route increased significantly. The TCI fluctuated upwards, with the cumulative increase of 0.58%. From Dec.11-Dec.12 (Thur.-Fri.), the freight rates in European route, Mediterranean route, American route and and Indian route continued to climb, and the freight rate in South American East route stopped falling and rebounded. The freight rates in South American West route and Central and South American route kept steady. The TCI increased rapidly, with the cumulative increase of 2.03%.

Finally, the TCI closed at 1159.03 points, with the cumulative increase of 29.58 points (2.62%) from Dec.5 (the last release day of Week 49).

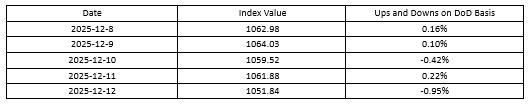

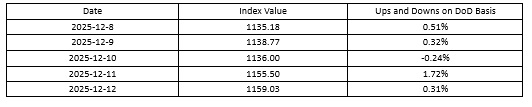

The TCI index value and several ups and downs on a day-on-day basis are as follows:

The TCI includes 19 sample routes. The main route analysis of this week is as follows:

European/Mediterranean route The strikes at the ports of Rotterdam, Antwerp, and Piraeus continued, and the market was in a period of long-term transportation agreement negotiations, providing support for rising freight rates. Coupled with factors such as increased transportation demand near New Year’s Day, shipping companies continued to raise freight rates this week. The freight indices in European route, Mediterranean East route and Mediterranean West route closed at 687.82 points, 991.14 points and 1271.52 points, with the increase of 2.49%, 6.47% and 6.73% on a week-on-week basis.

American route Market capacity remained high, with intense competition for cargo sources. In early this week, shipping companies significantly reduced rates to secure bookings. A fire at the Port of Los Angeles impacted container vessel operations, prompting some carriers to raise the freight rate for the American West Coast route in mid-to-late week, while the freight rate for the American East Coast route increased slightly. The freight index in American West Coast route closed at 736.81 points, with the increase of 1.16% on a week-on-week basis. The freight index in American East Coast route closed at 700.07 points, with the decrease of 1.64% on a week-on-week basis.

South American route Traders’ shipment volumes remained at a low level, with shipping capacity spilling over from the American route to the South American route, leading to a significant drop in freight rates for the South American route this week. The freight indices in South American West route, South American East route and Central and South American route closed at 773.68 points, 1003.03 points and 911.33 points, with the decrease of 5.45%, 2.86% and 9.03% on a week-on-week basis.

Indian route In the early stage, shipping companies continued to reduce their voyages, leading to a tightening of market capacity. In addition, some shippers concentrated on shipping recently, which drove a significant increase in the freight rate this week. The freight index in the Tianjin-India route closed at 967.66 points, with the increase of 10.38% on a week-on-week basis.

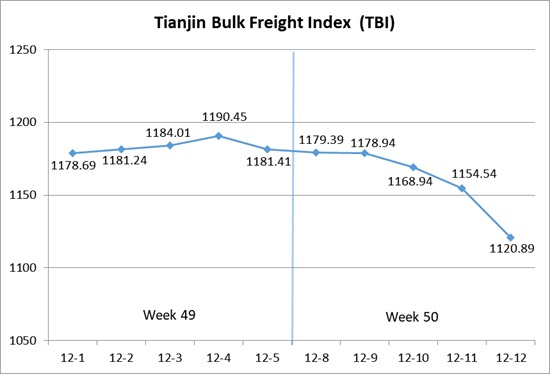

III. Tianjin Bulk Freight Index (TBI)

In Week 50, 2025 (Dec.8 to Dec.12), the trend of Tianjin Bulk Freight Index (TBI) was released as shown as follows:

In Week 50, the TBI dropped significantly.From Dec.8 to Dec.9 (Mon. to Tue.), coal market freight rates remained stable overall, while grain and metal ore market freight rates fluctuated within a narrow range, and TBI fell slightly, with a cumulative decline of 0.21%. From Dec.10 to Dec.12 (Wed. to Fri.), grain market freight rates continued to fell slightly, and coal and metal ore market freight rates slumped sharply. The TBI declined obviously and finally closed at 1120.89 points, with a cumulative decrease of 60.52 points or 5.12% compared to Dec.5 (the last release day of Week 49).

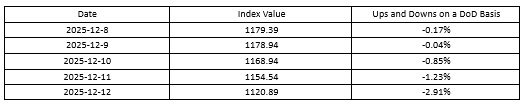

The TBI index value and several ups and downs on a day-on-day basis are as follows:

Tianjin Bulk Coal Freight Index (TBCI) Closed at 864.55 points, a cumulative decrease of 34.05 points or 3.79% compared to Dec.5 (the last release day of Week 49). Domestic coal import demand slowed down, leading to a decline in market freight rates. In terms of the supramax market, Indonesian coal cargo parcels were limited, and shipping capacity supply and demand were basically balanced. The freight index from the Indonesia to Qingdao route decreased by 0.66% on a weekly basis. In terms of the Capesize market, freight rates dropped sharply, with the freight index for the Hay Point to Qingdao route decreasing by 5.50% on a weekly basis.

Tianjin Bulk Grain Freight Index (TBGI) Closed at 927.44 points, a cumulative decrease of 11.97 points or 1.27% compared to Dec.5 (the last release day of Week 49). South American grain cargo parcels continued to decrease, and the supporting role of coal cargo parcels in the Panamax market was also weak, resulting in continuous declines in market freight rates. The freight index for the South America to Tianjin route decreased by 1.83% on a weekly basis, the index for the US Gulf to Tianjin route decreased by 1.02% on a weekly basis, and the index for the West America to Tianjin route decreased by 0.69% on a weekly basis.

Tianjin Bulk Mineral Freight Index (TBMI) Closed at 1570.69 points, a cumulative decrease of 135.53 points or 7.94% compared to Dec.5 (the last release day of Week 49). In terms of iron ore, major Australian and Brazilian miners slowed down shipments, market shipping capacity was in surplus, and freight rates continued to decline with an expanded week-on-week drop. The freight index for the Western Australia to Northern China route decreased by 9.20% on a weekly basis, and the index for the Brazil to Tianjin route decreased by 6.69% on a weekly basis. In terms of nickel ore, the freight index for the Surigao to Tianjin route slightly decreased, with a cumulative decline of 1.30% this week.

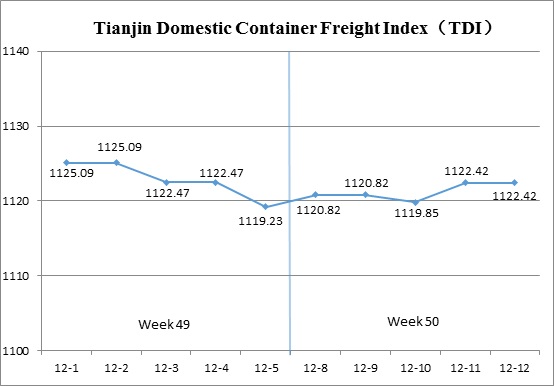

IV. Tianjin Domestic Container Freight Index (TDI)

In Week 50 (Dec.8 to Dec.12), the trend of the Tianjin Domestic Container Freight Index (TDI) is shown in the chart below:

In Week 50, the Tianjin Domestic Container Freight Index saw a slight rebound.

On Dec.8 (Mon.), the inbound index rose modestly, driving a slight increase in the TDI, which then stabilized. From Dec.10 to 11 (Wed. to Thur.), the inbound index continued its upward trend, while the outbound index saw a series of small declines, causing the TDI to dip before recovering. On Dec.12 (Fri.), both inbound and outbound indices remained stable, and the TDI ultimately closed at 1122.42 points, a 3.19-point increase, or a 0.29% rise, compared to Dec.5 (the last release day of Week 49).

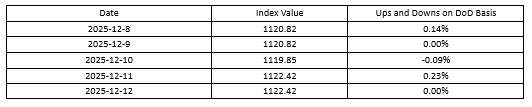

The TDI index value and several ups and downs on a day-on-day basis are as follows:

The Tianjin Domestic Container Outward Freight Index (TDOI) Continued its decline, closing at 1182.97 points on Dec.12, a 14.76-point decrease or a 1.23% drop compared to December 5 (the last release day of Week 49). In the Tianjin outbound domestic container market, cargo volumes decreased, and rates to southern China continued to decline. Rates to Fujian also saw a slight decrease. The Tianjin to Guangzhou route and Tianjin to Quanzhou/Xiamen routes saw their freight indices fall to 1140.27 points and 1444.74 points, respectively, with week-on-week drops of 1.33% and 1.35%. Rates to the East China region remained stable, with the Tianjin to Shanghai route freight index maintaining a steady 1103.09 points, unchanged from the previous week.

The Tianjin Domestic Container Inward Freight Index (TDII) Rebounded after a previous decline, reaching 1061.86 points on Dec.12, a 21.13-point increase or 2.03% growth compared to Dec.5 (the last release day of Week 49). Operations at Nansha Port remained stable, with an increase in vessel traffic. Although inbound freight rates are still lower compared to the same period last year, rates to East China, Fujian, and East China to Tianjin showed signs of recovery this week. The freight indices for the Shanghai to Tianjin route, Quanzhou/Xiamen to Tianjin route, and Guangzhou to Tianjin route closed at 1049.39 points, 807.97 points, and 1127.06 points, respectively, with week-on-week increases of 4.80%, 3.75%, and 1.38%.

(The analysis report is for reference only and at your own risk)